The Earned Income Tax Credit (EITC) is one of the most valuable tax credits available to low- and moderate-income workers in the United States. It was created to support working individuals and families by reducing their federal tax burden and, in many cases, providing a refund even when little or no income tax is owed. Because the credit is refundable, it can provide direct financial assistance to households that are actively participating in the workforce but still earning limited income. Every year, millions of taxpayers benefit from the Earned Income Tax Credit, and billions of dollars are distributed through this program to help families cover essential living expenses such as housing, food, transportation, childcare, education, and healthcare.

However, not every taxpayer automatically qualifies for this credit. The Internal Revenue Service (IRS) has established a detailed set of EITC eligibility requirements that must be satisfied before the credit can be claimed. These requirements are designed to ensure that the benefit reaches the workers and families who need it most while preventing improper claims. The rules involve several important factors, including earned income, filing status, Social Security number verification, residency conditions, investment income limits, and specific criteria for qualifying children. Understanding these rules is essential because claiming the credit incorrectly may result in delayed refunds, denied claims, repayment obligations, or even penalties imposed by the IRS.

Understanding the Earned Income Tax Credit

The Earned Income Tax Credit is a federal tax benefit designed to support workers who earn income through employment or self-employment but fall within certain income limits. Unlike tax deductions that simply reduce taxable income, the EITC directly reduces the amount of tax owed and may also result in a refund. This means that even taxpayers who owe no federal income tax can still receive money back from the government if they qualify for the credit.

The amount of the Earned Income Tax Credit varies depending on several factors. These include the taxpayer’s earned income, filing status, and the number of qualifying children listed on the tax return. Generally, families with children receive larger credits because the program is structured to support households with dependents. However, workers without children may also qualify under certain conditions, although the credit amount available to them is typically smaller.

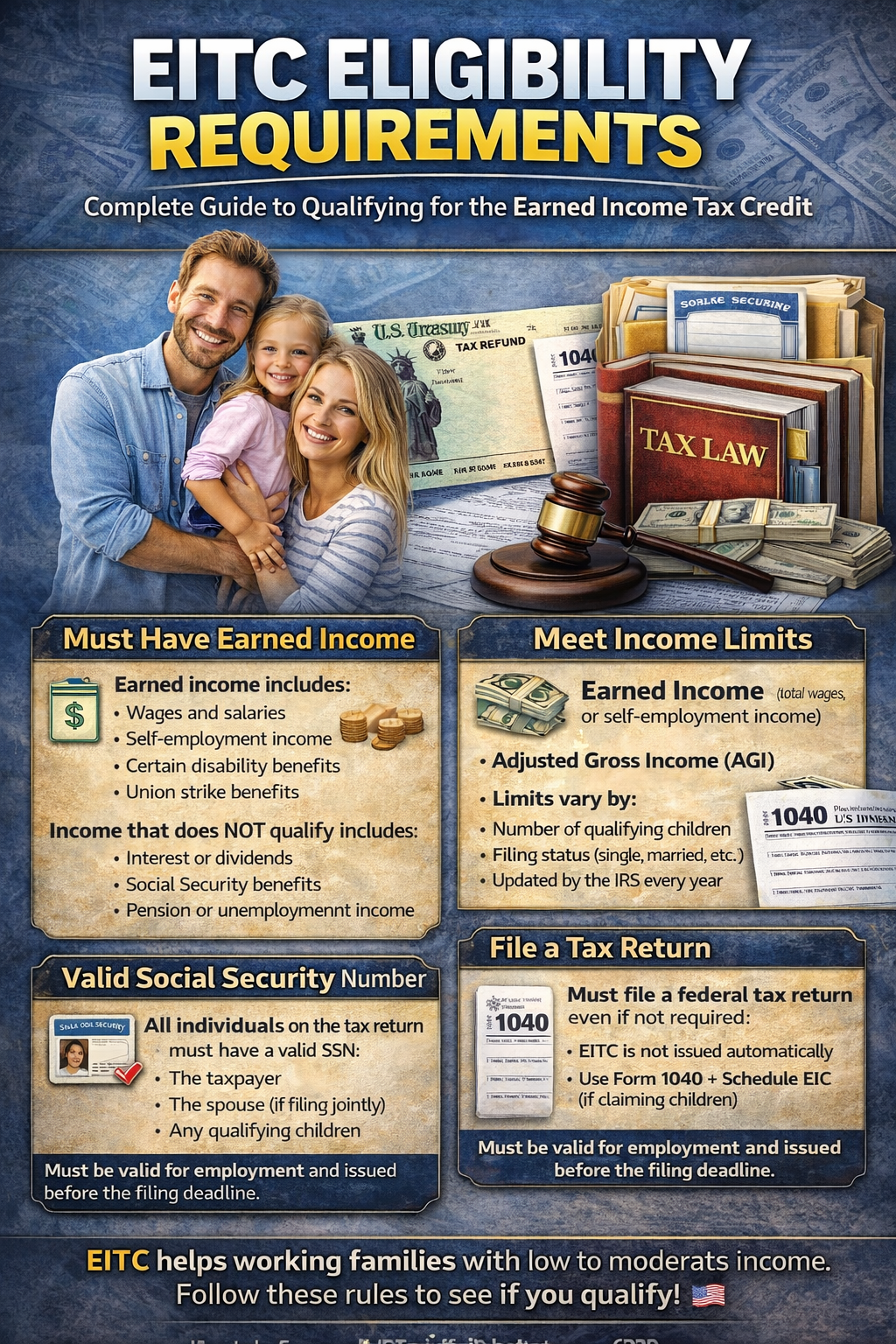

The EITC must be claimed when filing a federal income tax return, usually using Form 1040. If the taxpayer is claiming one or more qualifying children, additional information must be provided through Schedule EIC, which verifies the eligibility of each child listed on the return. Because the credit can significantly increase a tax refund, the IRS carefully reviews many EITC claims to ensure that all eligibility requirements have been satisfied.

Earned Income Requirement

One of the most fundamental eligibility rules for the Earned Income Tax Credit is that the taxpayer must have earned income during the tax year. Earned income refers to money that is received through active work or services performed for an employer or through self-employment. Because the purpose of the EITC is to encourage and support employment, the credit is only available to individuals who earn income through work.

Earned income typically includes wages, salaries, and tips received from an employer. It may also include income earned through self-employment, such as operating a small business, freelancing, or performing contract work. In some cases, certain disability benefits received before reaching retirement age may also be considered earned income for the purpose of claiming the credit. Additionally, union strike benefits and other forms of compensation related to employment may qualify as earned income under IRS guidelines.

However, many types of income are not considered earned income and therefore do not qualify for the Earned Income Tax Credit. Examples of non-qualifying income include interest from bank accounts, dividends from investments, pension payments, Social Security retirement benefits, unemployment compensation, and income received through inheritance or gifts. Since these forms of income are not related to active work, they do not meet the eligibility requirement for the EITC.

Income Limits for EITC Eligibility

Another important requirement for claiming the Earned Income Tax Credit involves meeting specific income limits established by the IRS. These limits ensure that the credit is directed toward taxpayers with low or moderate income levels. To qualify, both the taxpayer’s earned income and their Adjusted Gross Income (AGI) must fall below the maximum thresholds set by the IRS for the applicable tax year.

The income limits vary depending on the taxpayer’s filing status and the number of qualifying children listed on the tax return. Generally, households with more qualifying children are allowed higher income levels while still remaining eligible for the credit. For example, a taxpayer with three qualifying children may qualify for the EITC at a higher income level than a taxpayer with no children.

These income thresholds are adjusted periodically to account for inflation and changes in economic conditions. As a result, the exact limits may vary slightly from year to year. Taxpayers who are close to the income limit should review the most recent IRS guidelines to determine whether they remain eligible to claim the credit.

Social Security Number Requirement

To claim the Earned Income Tax Credit, the taxpayer must have a valid Social Security Number (SSN) issued by the Social Security Administration. This requirement applies not only to the taxpayer but also to the taxpayer’s spouse if filing a joint return and to any qualifying children listed on the tax return. The Social Security Number must be valid for employment and must be issued before the tax filing deadline for the applicable tax year.

This rule is designed to ensure accurate identification of taxpayers and to prevent fraudulent claims. Individuals who file taxes using an Individual Taxpayer Identification Number (ITIN) instead of a Social Security Number are generally not eligible to claim the Earned Income Tax Credit. Because of this requirement, taxpayers should verify that all Social Security Numbers included on their tax return are accurate and valid before submitting their return to the IRS.

Filing Status Rules

The taxpayer’s filing status also plays a significant role in determining eligibility for the Earned Income Tax Credit. Most filing statuses are eligible to claim the credit, including Single, Married Filing Jointly, Head of Household, and Qualifying Widow or Widower. However, taxpayers who file their returns using the Married Filing Separately status are not eligible to claim the EITC under normal circumstances.

Choosing the correct filing status is important because it affects both eligibility and the amount of the credit that may be received. For example, married couples who file jointly may qualify for higher income limits compared to individuals filing as single taxpayers. Therefore, understanding how filing status affects EITC eligibility can help taxpayers maximize the benefits available to them.

Residency and Citizenship Requirements

The Earned Income Tax Credit is intended primarily for individuals who live and work in the United States. Therefore, taxpayers must generally be U.S. citizens or resident aliens for the entire tax year to qualify for the credit.

In cases where a taxpayer is married to a nonresident alien spouse, the couple must typically file a joint return and choose to treat the nonresident spouse as a U.S. resident for tax purposes in order to claim the EITC. This rule ensures that the credit is directed toward individuals who participate in the U.S. workforce and contribute to the U.S. tax system.

Investment Income Limit

In addition to earned income limits, the IRS also places a restriction on investment income for taxpayers claiming the Earned Income Tax Credit. Investment income includes earnings generated from financial assets rather than employment. Examples include interest from savings accounts, dividends from stocks, capital gains from the sale of investments, rental property income, and royalties from intellectual property.

If a taxpayer’s investment income exceeds the maximum limit established by the IRS for the tax year, the taxpayer becomes ineligible for the EITC regardless of their earned income level. This rule prevents individuals with substantial financial investments from claiming a credit that is intended to assist workers with limited resources.

Special Rules for Taxpayers Without Children

Although the Earned Income Tax Credit is commonly associated with families who have children, individuals without children may also qualify under certain conditions. However, stricter eligibility rules apply to taxpayers who do not have qualifying children.

For example, taxpayers without children must generally be at least 25 years old but younger than 65 years old at the end of the tax year. They must also live in the United States for more than half of the year. Additionally, they cannot be claimed as a dependent by another taxpayer.

Qualifying Child Requirements

Taxpayers who claim children for the Earned Income Tax Credit must ensure that each child meets several eligibility tests established by the IRS. These tests include the relationship test, age test, residency test, and joint return test.

The relationship test requires that the child be closely related to the taxpayer, such as a son, daughter, stepchild, adopted child, foster child placed by an authorized agency, sibling, or a descendant of one of these individuals.

The age test requires that the child be under age 19 at the end of the tax year, under age 24 if the child is a full-time student, or any age if the child is permanently and totally disabled.

The residency test requires that the child live with the taxpayer in the United States for more than half of the tax year, although certain temporary absences such as school attendance or medical care may still count as living with the taxpayer.

Frequently Asked Questions (FAQs)

Who qualifies for the Earned Income Tax Credit (EITC)?

Workers with low to moderate income may qualify for the Earned Income Tax Credit if they meet several IRS requirements. These include having earned income from employment or self-employment, meeting income limits set for the tax year, having a valid Social Security number, and using an eligible filing status. Taxpayers may qualify with or without qualifying children, but those with children usually receive a larger credit amount. In addition, the taxpayer must generally be a U.S. citizen or resident alien for the entire tax year and cannot be claimed as a dependent by another taxpayer.

Can you claim the EITC without having children?

Yes, it is possible to claim the Earned Income Tax Credit without qualifying children, but stricter rules apply. The taxpayer must typically be at least 25 years old but younger than 65 years old at the end of the tax year. They must also live in the United States for more than half of the year and cannot be claimed as a dependent on another person’s tax return. Because these additional restrictions apply, the credit amount available to taxpayers without children is generally smaller compared to families with qualifying children.

What income qualifies as earned income for the EITC?

Earned income includes wages, salaries, tips, and other compensation received for performing work for an employer. Income earned from self-employment, freelancing, and operating a small business may also qualify as earned income. Certain disability benefits received before retirement age may count as well. However, some types of income do not qualify as earned income for the EITC. These include interest income, dividends, pensions, Social Security retirement benefits, unemployment compensation, and other forms of passive income that are not related to active work.

Can you claim the EITC if you are married?

Yes, married couples may qualify for the Earned Income Tax Credit if they meet all eligibility requirements and file their taxes using the Married Filing Jointly status. Couples who file using the Married Filing Separately status generally cannot claim the credit. Filing jointly may allow married taxpayers to qualify under higher income limits compared to single taxpayers, especially if they have qualifying children. It is important for married couples to review the income thresholds and eligibility rules carefully when determining whether they qualify for the credit.

What happens if the IRS denies an EITC claim?

If the IRS denies an Earned Income Tax Credit claim, the taxpayer may be asked to provide additional documentation proving eligibility. This could include documents verifying income, residency of a qualifying child, or relationship to the child listed on the tax return. If the claim is determined to be incorrect, the taxpayer may be required to repay the credit and may face penalties or restrictions on claiming the EITC in future tax years. For this reason, it is important to review all eligibility requirements carefully before filing a tax return that includes the credit.

Reference Links

https://www.irs.gov/credits-deductions/individuals/earned-income-tax-credit-eitc

https://www.irs.gov/publications/p596

https://www.taxpolicycenter.org/briefing-book/what-earned-income-tax-credit

https://www.cbpp.org/research/federal-tax/the-earned-income-tax-credit

https://www.irs.gov/credits-deductions/eitc-income-limits

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official authorities.