Tax credits are among the most powerful financial tools available within any tax system, yet they are often misunderstood, underused, or confused with other tax benefits such as deductions and exemptions. Many taxpayers hear the term “tax credit” during tax season, but the real meaning, long-term financial impact, and strategic value of these credits are not always fully understood. As a result, significant amounts of money are left unclaimed every year simply because individuals and families do not realize what they qualify for or how these credits actually work.

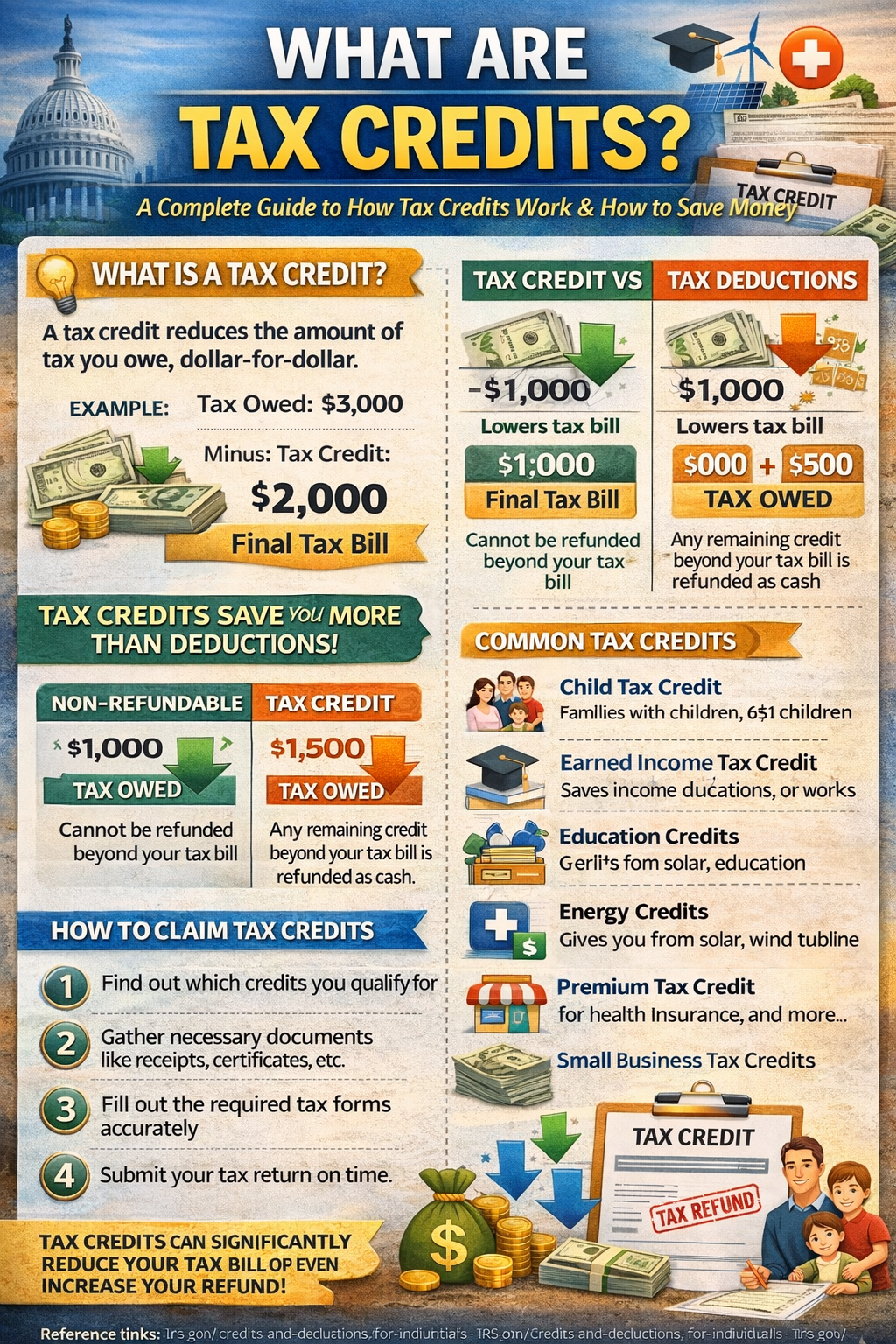

In simple terms, a tax credit is an amount of money that is subtracted directly from the total tax owed to the government. Unlike deductions, which only reduce taxable income, tax credits reduce the final tax bill itself. This difference may seem small at first glance, but in financial terms, it is extremely powerful. A credit reduces taxes dollar for dollar. That means a $1,000 tax credit reduces your tax bill by $1,000 not just a percentage of it.

What Are Tax Credits?

A tax credit is defined as a financial incentive provided by the government that reduces the amount of income tax owed. This reduction is applied directly to the final tax liability rather than to taxable income. Because of this direct application, tax credits are generally considered more valuable than deductions of the same amount.

To better understand this, consider the following example. Suppose a person calculates their taxes and determines that $4,000 is owed to the government. If that person qualifies for a $1,500 tax credit, the final tax bill will be reduced to $2,500. The reduction is immediate and exact. It is not based on tax brackets or percentages. It is a direct subtraction.

Tax credits are typically introduced through legislation to encourage certain behaviors or to provide financial support to targeted groups. Governments use tax credits to influence economic decisions, promote social welfare, and stimulate growth in specific sectors. In many cases, these credits are designed to benefit families, students, homeowners, low-income workers, and businesses that invest in innovation or clean energy.

Why Governments Offer Tax Credits

Tax credits are not random financial gifts. They are policy tools designed with specific economic and social goals in mind. When governments introduce tax credits, long-term planning and economic strategy are usually involved.

One primary purpose of tax credits is financial relief. Families with children face higher costs for housing, food, education, and healthcare. Child-related tax credits are often designed to reduce this financial pressure and support family stability.

Another purpose is behavioral encouragement. Education credits are introduced to make college more affordable, thereby increasing the number of skilled workers in the economy. Energy credits encourage homeowners and businesses to invest in environmentally friendly technologies. Healthcare credits make insurance more accessible.

Economic stimulation is also a key reason. When individuals receive tax refunds or reduced tax bills, disposable income increases. That money is often spent in local economies, supporting small businesses and job growth. During economic downturns, refundable tax credits are frequently expanded to inject money directly into households.

The Critical Difference Between Tax Credits and Tax Deductions

Tax credits and tax deductions are often confused, yet they operate in fundamentally different ways. Understanding this distinction is essential for making informed financial decisions.

A tax deduction reduces taxable income. For example, if an individual earns $60,000 per year and qualifies for a $5,000 deduction, the taxable income becomes $55,000. The tax savings depend on the person’s tax bracket. If the tax rate is 20%, the deduction results in a $1,000 savings (20% of $5,000).

A tax credit, however, reduces the tax owed directly. If the same individual owes $6,000 in taxes and qualifies for a $1,000 credit, the new tax bill becomes $5,000.

Types of Tax Credits Explained in Detail

Tax credits are generally classified into three major categories: non-refundable, refundable, and partially refundable. Each type has unique characteristics that influence how much benefit can be received.

Non-Refundable Tax Credits

A non-refundable tax credit can reduce the tax owed to zero, but it cannot result in a refund beyond that amount. If the credit exceeds the tax liability, the excess amount is lost.

For example, if $800 is owed in taxes and a $1,200 non-refundable credit is available, the tax bill will become zero, but the remaining $400 will not be refunded.

Refundable Tax Credits

Refundable tax credits are significantly more powerful. They can reduce the tax bill to zero and provide a refund for any remaining credit amount.

One well-known example is the Earned Income Tax Credit, which supports low- and moderate-income workers. If an eligible taxpayer qualifies for a credit larger than the tax owed, the difference is refunded.

Partially Refundable Tax Credits

Partially refundable credits allow a portion of the unused credit to be refunded. The refundable portion is usually capped at a specific amount.

Common Examples of Tax Credits

Several tax credits are commonly claimed by individuals and families.

The Child Tax Credit provides financial support for families with dependent children. Income limits and age requirements typically apply.

The Lifetime Learning Credit supports ongoing education and skill development.

Clean energy improvements are supported under policies expanded by the Inflation Reduction Act, which increased incentives for renewable energy installations.

Healthcare affordability has been improved through subsidies under the Affordable Care Act, which provides premium tax credits to eligible individuals.

How Businesses Benefit From Tax Credits

Tax credits are not limited to individuals. Businesses also receive powerful incentives.

Credits may be available for:

-

Research and development investments

-

Hiring veterans or disadvantaged workers

-

Installing renewable energy systems

-

Providing employee healthcare coverage

These incentives encourage innovation, job creation, and long-term economic growth.

Frequently Asked Questions (FAQs)

Are tax credits available to everyone?

No. Most tax credits have eligibility requirements, including income limits, dependent status rules, or specific expense qualifications. Each credit has its own guidelines.

Can I claim multiple tax credits in one year?

Yes. If eligibility requirements are met, multiple credits may be claimed in the same tax year. For example, a family may qualify for both a child tax credit and an education credit.

What happens if I make too much money?

Many credits include income phase-outs. As income increases beyond certain thresholds, the credit amount gradually decreases until it is eliminated.

Do tax credits change every year?

Yes. Credit amounts, eligibility rules, and refundability provisions can change through new legislation or policy adjustments.

Can tax credits be audited?

Yes. Governments may review claims, especially for refundable credits. Documentation must be maintained.

Are tax credits better than tax refunds?

A tax credit can lead to a refund, but they are not the same. A refund occurs when payments exceed final tax liability. Credits reduce the liability itself.

How can I find out which credits I qualify for?

Official government tax websites, professional tax advisors, and updated tax software are recommended sources.

Can tax credits reduce self-employment tax?

Generally, credits reduce income tax liability, but some specialized credits may interact with other tax components.

What is an income phase-out?

An income phase-out is a gradual reduction of a credit as income rises beyond a specific level.

Why are refundable credits considered anti-poverty tools?

Because they provide financial support even when no tax is owed, refundable credits increase income for lower-income households.

Reference Links

Internal Revenue Service – Credits and Deductions https://www.irs.gov/credits-deductions-for-individuals

Earned Income Tax Credit (EITC) https://www.irs.gov/credits-deductions/individuals/earned-income-tax-credit

Child Tax Credit https://www.irs.gov/credits-deductions/individuals/child-tax-credit

American Opportunity Tax Credit https://www.irs.gov/credits-deductions/individuals/aotc

Lifetime Learning Credit https://www.irs.gov/credits-deductions/individuals/llc

Affordable Care Act Premium Tax Credit https://www.healthcare.gov/glossary/premium-tax-credit/

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official housing authorities.