The PPP loan, officially known as the Paycheck Protection Program, was one of the most important financial relief programs ever created for small businesses in the United States. It was introduced during a time of fear, uncertainty, and economic shutdown caused by the COVID-19 pandemic. For many business owners, the PPP loan was not just helpful it was the reason their business survived.

What Was the PPP Loan?

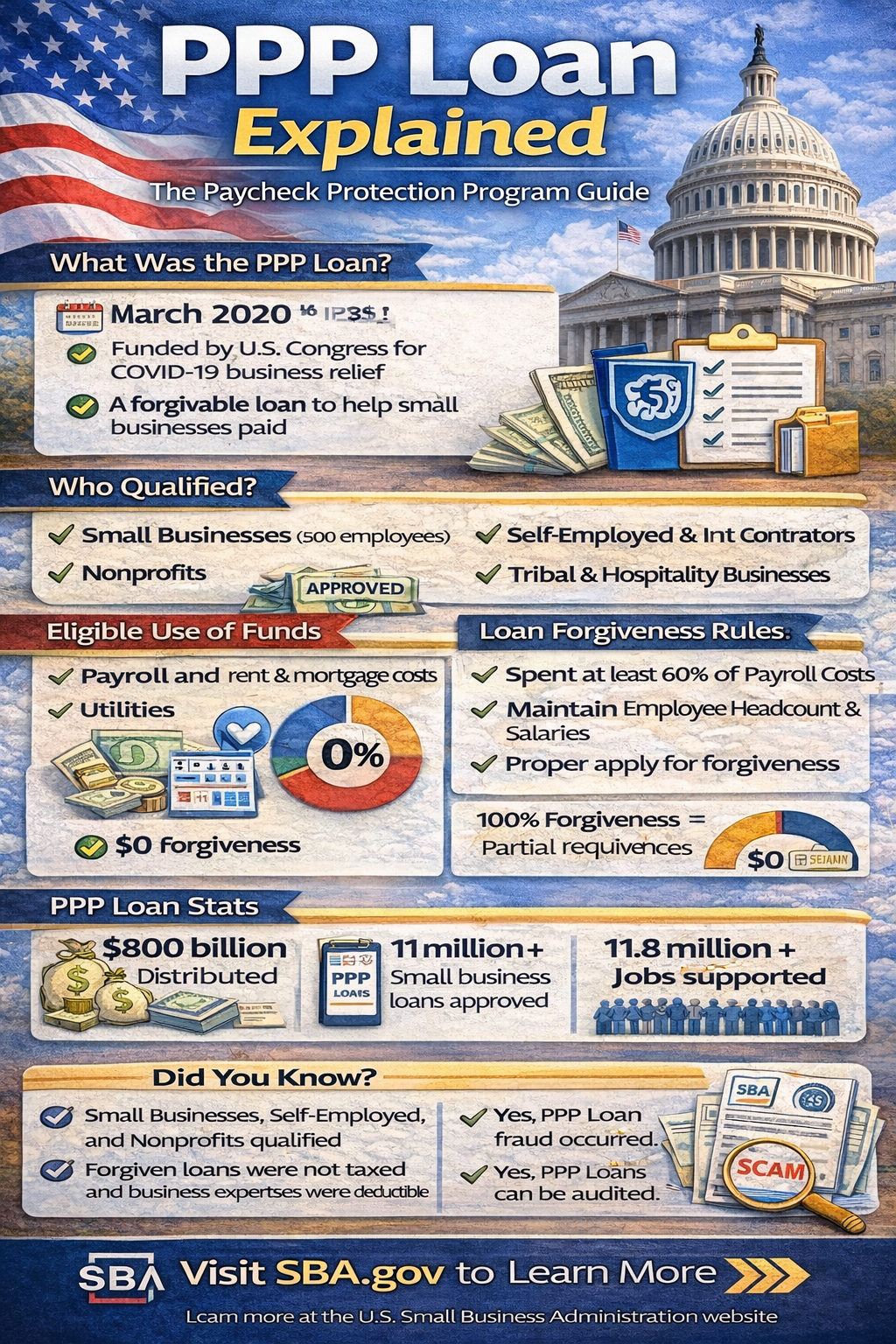

The PPP loan was created in March 2020 as part of a massive emergency response to the COVID-19 economic crisis. When lockdowns began across the United States, businesses of all sizes suddenly lost customers, revenue, and stability. Small businesses were hit the hardest because most of them operate with limited savings and depend on daily or weekly income to survive. Without immediate help, millions of workers were at risk of losing their jobs, and countless small businesses faced permanent closure.

To prevent economic collapse, the U.S. government passed the CARES Act, which included the Paycheck Protection Program. The main goal of the PPP loan was simple but powerful: keep employees on payroll and help businesses continue paying basic operating expenses during the crisis. Unlike traditional business loans, the PPP loan was designed to be forgivable, meaning that if businesses followed the rules, the money would not need to be repaid.

The program was administered by the U.S. Small Business Administration (SBA) in partnership with private lenders such as banks, credit unions, and online financial institutions. This public-private partnership allowed the government to distribute money quickly to millions of businesses across the country.

How the PPP Loan Was Different from Normal Business Loans

Traditional business loans usually involve strict credit checks, collateral requirements, long approval timelines, and full repayment with interest. During a national emergency, this model would have failed because businesses needed money immediately, not months later.

The PPP loan worked differently. Credit scores were not the main factor. Collateral was not required. Personal guarantees were not required. Most importantly, loan forgiveness was built directly into the program. If a business used the funds correctly mainly to pay employees the loan could be fully forgiven.

Who Was Eligible for a PPP Loan?

Eligibility for the PPP loan was broader than many people expected, especially during the early stages of the program. The intention was to include as many struggling small businesses as possible.

Businesses and organizations that were generally eligible included small businesses with 500 or fewer employees, sole proprietors, independent contractors, self-employed individuals, nonprofit organizations, veterans’ organizations, and tribal businesses. Some businesses with more than 500 employees were also eligible if they met specific industry size standards set by the SBA.

To qualify, businesses had to certify that economic uncertainty made the loan necessary to support ongoing operations. This requirement later became controversial, especially when large companies applied for PPP loans, but for most small businesses, the need was real and immediate.

How PPP Loan Amounts Were Calculated

The amount of money a business could receive through the PPP loan was based primarily on payroll costs. In most cases, businesses could borrow up to 2.5 times their average monthly payroll expenses. This formula was designed to provide approximately eight to ten weeks of payroll support.

Payroll costs included employee wages, salaries, tips, paid leave, health insurance benefits, retirement contributions, and state payroll taxes. However, individual employee compensation was capped at an annualized salary of $100,000, meaning higher-paid employees could not inflate loan amounts.

How PPP Loan Funds Were Allowed to Be Used

PPP loan funds came with strict usage rules, especially for businesses seeking full forgiveness. At least 60% of the loan had to be used for payroll costs, including employee wages and benefits. The remaining 40% could be used for approved non-payroll expenses.

Approved non-payroll expenses included rent, mortgage interest, utilities, business software, certain supplier costs, and expenses related to health and safety improvements. Over time, the government expanded the list of eligible expenses to make the program more flexible and practical for businesses facing different challenges.

PPP Loan Forgiveness Explained Clearly

Loan forgiveness was the most important and confusing part of the PPP program for many business owners. Forgiveness meant that the SBA would repay the loan on behalf of the borrower, effectively turning the loan into free money.

To qualify for full forgiveness, businesses had to meet several conditions. They had to use the funds during the covered period, spend at least 60% on payroll, maintain employee headcount, and avoid significantly reducing employee wages. Businesses also had to submit documentation proving how the money was used.

The Role of the PPP Flexibility Act

As businesses struggled to meet early PPP requirements, Congress passed the Paycheck Protection Program Flexibility Act. This law made the program more realistic and forgiving.

It extended the covered period from eight weeks to twenty-four weeks, reduced payroll spending requirements, and extended loan repayment terms. These changes allowed more businesses to qualify for forgiveness and better reflected the long-lasting impact of the pandemic.

First-Draw and Second-Draw PPP Loans

The PPP program was rolled out in phases. The first phase, known as First-Draw PPP loans, was available to eligible businesses that had not previously received PPP funding.

The second phase, called Second-Draw PPP loans, targeted businesses that were still struggling after using their first loan. To qualify, businesses had to demonstrate at least a 25% reduction in revenue and meet stricter employee limits. This approach focused aid on businesses that needed it the most.

Tax Treatment of PPP Loans

One of the biggest concerns among business owners was how PPP loans would be treated for tax purposes. Initially, there was confusion and uncertainty.

Eventually, Congress clarified that forgiven PPP loans were not taxable income, and businesses could still deduct eligible expenses paid with PPP funds. This decision significantly increased the financial value of the program and reduced tax stress for struggling businesses.

Mistakes and Risks

Despite its benefits, the PPP program also revealed weaknesses. Some businesses misunderstood the rules, failed to keep proper records, or used funds incorrectly. In more serious cases, fraud occurred, with individuals submitting false applications or inflating payroll numbers.

The government later launched investigations and audits, especially for larger loans. These actions highlighted the importance of honesty, transparency, and documentation when dealing with government relief programs.

Economic Impact

The PPP loan program distributed over $800 billion and supported millions of jobs across the United States. While it was not perfect, most economists agree that it prevented a deeper and longer-lasting economic collapse.

Small businesses were able to keep employees, pay rent, and survive until restrictions eased. Communities benefited from reduced unemployment and greater economic stability during an unprecedented crisis.

Frequently Asked Questions (FAQs)

Is the PPP loan still available?

No. The PPP application period officially ended in May 2021.

Do PPP loans need to be repaid?

Only if they were not fully forgiven.

Can PPP loans still be audited?

Yes. The SBA can review and audit loans, especially larger ones.

Did self-employed individuals qualify?

Yes. Independent contractors and sole proprietors were eligible.

Was PPP fraud punished?

Yes. Fraud cases have resulted in fines, repayments, and criminal charges.

Reference Links

Official overview of the Paycheck Protection Program https://www.sba.gov/funding-programs/loans/covid-19-relief-options/paycheck-protection-program

Full text and explanation of the CARES Act https://www.congress.gov/bill/116th-congress/house-bill/748

IRS guidance on PPP loan forgiveness and taxes https://www.irs.gov/newsroom/forgiveness-of-paycheck-protection-program-loans

U.S. Department of the Treasury COVID-19 relief programs https://home.treasury.gov/policy-issues/coronavirus

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official housing authorities.