Losing a loved one is one of the most painful experiences a family can face. During that time, financial stress can make everything even harder. That is why survivor benefits are so important. In the United States, Social Security survivor benefits are designed to provide monthly financial support to certain family members of a worker who paid Social Security taxes before death. These benefits can help replace part of the income that was lost and can support a surviving spouse, children, divorced spouse, or even dependent parents in some cases. The program exists to protect families after a death, but many people do not fully understand who qualifies, how much may be paid, when benefits can begin, or what steps must be taken to apply.

Survivor benefits are not the same as retirement benefits, even though both are administered by the Social Security Administration. They follow their own eligibility rules, age rules, filing rules, and payment formulas. A surviving spouse may be able to claim as early as age 60, or age 50 if disabled. A surviving spouse caring for the deceased worker’s child may qualify even earlier. Unmarried children may also be eligible, and in limited cases dependent parents may qualify as well. The amount paid depends on the deceased worker’s earnings record, the survivor’s relationship to that worker, and the age at which the survivor begins receiving payments. Social Security also provides a small lump-sum death payment in some cases. Official SSA guidance says survivor benefits may be available to a spouse, ex-spouse, child, or dependent parent of a worker who paid Social Security taxes before death.

What Are Survivor Benefits?

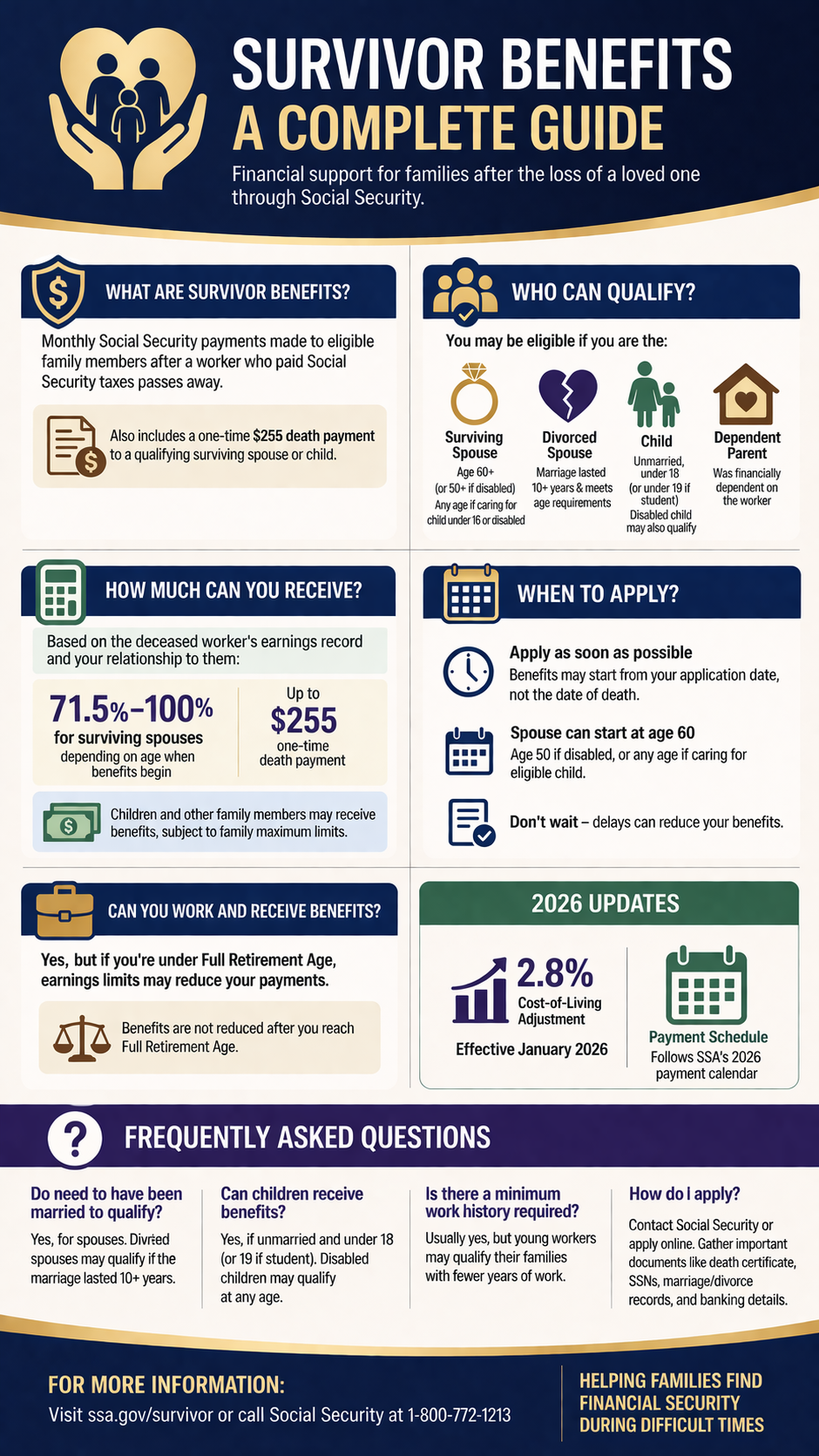

Survivor benefits are monthly Social Security payments made to eligible family members after a worker dies. These payments are based on the deceased worker’s earnings history and the Social Security taxes paid during that person’s working years. The purpose is simple: if a household depended partly or fully on the worker’s income, Social Security may provide continuing support to qualified survivors after that income ends. SSA states that survivor benefits provide monthly payments to eligible family members of people who worked and paid Social Security taxes before they died.

Many people assume a worker must have spent decades in the workforce before any survivor can qualify, but that is not always true. The number of work credits needed depends partly on the worker’s age at death. In general, younger workers need fewer years of work for their families to become eligible. SSA explains that no one needs more than 10 years of work for any Social Security benefit, and under a special rule, benefits may be payable to children and a spouse caring for those children even with a shorter work history.

Survivor benefits are often semantically connected to topics such as widow benefits, widower benefits, Social Security death benefits, benefits for surviving spouses, benefits for children of deceased workers, and dependent parent survivor payments. These related phrases matter because people often search for the same topic using different words. In practical terms, they all lead back to the same core question: when a worker dies, can the surviving family receive financial help from Social Security?

Who Can Qualify for Survivor Benefits?

The Social Security Administration says survivor benefits may be available to a surviving spouse, surviving divorced spouse, unmarried child, or dependent parent of a deceased worker who paid Social Security taxes before death. This broad category includes several groups, and each one follows its own rules.

A surviving spouse may qualify if the marriage requirements are met and the spouse files at the appropriate age or qualifies through caregiving or disability rules. A widow or widower can generally begin survivor benefits at age 60, or at age 50 if disabled. SSA also says a surviving spouse may qualify at any age when caring for the deceased worker’s child who is under 16 or has a disability and is receiving benefits on the worker’s record.

A surviving divorced spouse may also qualify. In general, this usually requires that the marriage lasted at least 10 years and that the ex-spouse meets the age or caregiving rules that apply to surviving spouses. This is an important rule because many divorced people wrongly assume they lose all access to benefits connected to a former spouse’s record after death. In some cases, they do not.

A child may qualify if the child is unmarried and meets age or disability rules. A deceased worker’s biological child, adopted child, stepchild, or, in some situations, grandchild may qualify. Children are often eligible if they are under 18, or up to 19 if still attending elementary or secondary school full time. Adult children with disabilities may also qualify if the disability began before age 22 and other rules are met. SSA identifies children as one of the main categories that may qualify for survivor benefits.

How the Deceased Worker Qualifies a Family

A family cannot receive survivor benefits unless the deceased person had sufficient Social Security coverage. This usually means the worker earned enough work credits by paying Social Security taxes through employment or self-employment. SSA explains that the number of years needed depends on the worker’s age when they die, and that younger workers may qualify their families with fewer years of work. No one needs more than 10 years of work to qualify family members for Social Security survivors benefits.

This matters because many younger families think they are automatically ineligible if the deceased worker had not yet built a long career. That is not always correct. If the worker was relatively young, survivor protection may still exist. Families should not assume they are disqualified without checking SSA rules or contacting the agency directly.

How Much Can Survivors Receive?

The amount a survivor can receive depends on the deceased worker’s earnings record and on which family member is filing. Different survivor categories receive different percentages. SSA states that a surviving spouse can receive between 71.5% and 100% of the deceased spouse’s benefit, depending on age at filing. The amount generally increases the longer the spouse waits, up to full retirement age for survivor benefits.

Full retirement age for survivor benefits is not always the same as full retirement age for a worker’s own retirement benefits. SSA says survivor full retirement age is between 66 and 67, depending on year of birth, and it is the age at which the maximum survivor benefit can be paid. This distinction is very important because some people think the retirement and survivor age rules are identical, but they are not.

Children who qualify can receive benefits as well, and multiple family members can sometimes receive benefits on the same worker’s record. However, Social Security family maximum rules may limit the total amount payable to the family each month. That means even if several people qualify, the total amount paid on one record may be capped and then divided among eligible survivors. The exact distribution depends on SSA calculations.

Survivor Benefits for a Spouse

A surviving spouse is the category most people think about first, and for good reason. Widow and widower benefits can provide meaningful monthly support. In general, a surviving spouse may start benefits at age 60, or at age 50 if disabled. A spouse caring for the deceased worker’s child under 16 or a child with a disability may be eligible regardless of age.

The age at which a spouse files matters a lot. If benefits begin earlier than survivor full retirement age, the monthly payment is reduced. If the spouse waits until survivor full retirement age, the payment can reach the maximum survivor amount allowed under SSA rules. According to SSA’s 2026 blog guidance, a surviving spouse may receive from 71.5% to 100% of the deceased spouse’s benefit depending on filing age.

This creates an important planning question. Some surviving spouses choose to start survivor benefits earlier because they need income right away. Others delay because they want a larger monthly amount later. The best choice depends on age, health, work plans, other income sources, and whether the person may later switch between survivor benefits and their own retirement benefit.

Survivor Benefits for a Divorced Spouse

A surviving divorced spouse can sometimes receive benefits on a deceased ex-spouse’s record. This is one of the least understood parts of Social Security. In general, the former marriage must have lasted at least 10 years, and the surviving divorced spouse must meet SSA rules tied to age, marital status, and eligibility. While many people never realize this protection exists, it can be extremely valuable, especially when the ex-spouse had a stronger earnings record.

This does not reduce benefits for other survivors in the same way many people fear, and it is not treated as a private favor from the deceased person’s estate. It is part of Social Security law. Anyone who was divorced from a deceased worker after a long marriage should review the official eligibility rules carefully.

Survivor Benefits for Children

Children can be among the most important recipients of survivor benefits. If a parent dies, qualifying children may receive monthly payments that help support housing, food, education, and daily care. A child is generally eligible if unmarried and under age 18, or up to age 19 if still a full-time student in elementary or secondary school. Disabled adult children may qualify if the disability began before age 22 and the other SSA conditions are met. SSA includes children among the core groups eligible for survivor payments.

These benefits can be essential for single-parent households or for grandparents or relatives now caring for the child. In addition, a surviving spouse who is caring for the deceased worker’s child under 16 or with a disability may be eligible for spouse survivor benefits even before age 60.

Survivor Benefits for Parents

Although less common, dependent parents of a deceased worker may qualify for monthly survivor benefits if they were financially dependent on the worker. This can matter for older parents who relied on an adult son or daughter for support. The dependency requirements are specific, so parents should review SSA guidance or contact the agency to see whether they qualify.

Lump-Sum Death Payment

In addition to monthly survivor benefits, Social Security may pay a one-time lump-sum death payment, typically $255, to a qualifying surviving spouse or, if eligible, to a qualifying child. SSA’s death payment application form relates to this benefit. While this amount is small and does not cover major funeral costs, it is still a formal part of the survivor benefit system and should not be overlooked.

Working While Receiving Survivor Benefits

Some survivors continue working while receiving benefits. SSA says you can work and receive survivor benefits, but earnings limits apply if you are under full retirement age. This is an important point because work income can reduce current payments before full retirement age, though it does not always mean the money is permanently lost in the long run. The exact effect depends on annual earnings and SSA’s current earnings test rules.

This means a surviving spouse who is still employed should be very careful before filing early. A benefit that looks attractive on paper can be reduced if earnings exceed the applicable limit. On the other hand, someone with little or no work income may find early survivor benefits very helpful.

When to Apply for Survivor Benefits

SSA encourages people to apply as soon as they can because, for some claims, benefits are paid from the time of application and not from the time of death. That means delay can cost money. Families often spend the first weeks after a death dealing with grief, funeral arrangements, estate issues, and household changes, so Social Security paperwork may not feel urgent. Still, applying promptly is often wise.

The application process can depend on the category of survivor, and some claims may require a phone call or other direct contact with SSA. Before applying, it helps to gather identifying documents, the deceased worker’s Social Security number, marriage or divorce records if relevant, birth certificates for children, and banking details for direct deposit.

Payment Timing and 2026 Updates

Social Security announced a 2.8% cost-of-living adjustment for 2026, which affects Social Security benefits beginning in January 2026. Payment dates in 2026 also follow SSA’s published payment schedule, which varies by the beneficiary’s situation and birth date grouping. These details matter because people often ask not only whether they qualify, but also when money will arrive and whether payments changed in 2026.

Common Mistakes People Make About Survivor Benefits

A very common mistake is believing only elderly widows can qualify. In reality, survivor benefits can also apply to younger disabled spouses, spouses caring for children, children themselves, divorced spouses, and dependent parents. Another common mistake is assuming the deceased worker needed a full 10-year career in every case. SSA makes clear that younger workers may qualify their families with fewer years of work.

A third mistake is waiting too long to apply. Because some benefits are tied to the application date, waiting may reduce what the family ultimately receives. SSA specifically encourages people to apply as soon as they can.

FAQs About Survivor Benefits

Who can receive Social Security survivor benefits?

Social Security says survivor benefits may be available to a spouse, divorced spouse, child, or dependent parent of a worker who paid Social Security taxes before death. Eligibility depends on the relationship, age, disability status, dependency, and other SSA rules.

At what age can a widow or widower start survivor benefits?

A surviving spouse can generally start survivor benefits at age 60, or at age 50 if disabled. A spouse caring for the deceased worker’s child under 16 or a child with a disability may qualify at any age.

How much can a surviving spouse receive?

According to SSA, a surviving spouse can receive about 71.5% to 100% of the deceased spouse’s benefit, depending largely on the age at which benefits begin. Waiting until full retirement age for survivor benefits can increase the monthly amount.

Can children receive survivor benefits?

Yes. Unmarried children may qualify, generally if they are under 18, or up to 19 if still attending elementary or secondary school full time. Disabled adult children may also qualify if the disability began before age 22 and SSA conditions are met.

Is there a one-time Social Security death benefit?

Yes. Social Security may pay a one-time lump-sum death payment, usually $255, to a qualifying surviving spouse or child.

Can I work and still receive survivor benefits?

Yes, but if you are under full retirement age, earnings limits can apply and may reduce benefits. SSA says you can work and receive survivor benefits, but the earnings test matters before full retirement age.

Does a divorced spouse ever qualify for survivor benefits?

Yes, a surviving divorced spouse may qualify if SSA rules are met. One major rule is that the marriage generally must have lasted at least 10 years. The person must also meet the relevant age or caregiving conditions.

How soon should I apply after a death?

As soon as reasonably possible. SSA says some claims are paid from the time you apply, not from the time the worker died, so delays can cost benefits.

Reference Links

https://www.ssa.gov/survivor/

https://www.ssa.gov/survivor/eligibility

https://www.ssa.gov/survivor/amount

https://www.ssa.gov/survivor/full-retirement-age-survivor

https://www.ssa.gov/pubs/EN-05-10084.pdf

https://www.ssa.gov/blog/en/posts/2026-03-12.html

https://www.ssa.gov/marketing/assets/materials/EN-05-10402.pdf

https://www.ssa.gov/forms/ssa-8.pdf

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official authorities.