For many Americans, receiving a letter from the Internal Revenue Service (IRS) is enough to cause concern. When that letter contains the word “audit,” the anxiety often increases significantly. Taxpayers may immediately worry about penalties, back taxes, or legal consequences. However, an IRS audit is not necessarily a sign that something is wrong. In reality, audits are a routine part of tax administration and are designed to verify the accuracy of tax returns rather than punish taxpayers.

The IRS processes hundreds of millions of tax returns every year. While most returns are accepted without issue, some are selected for additional review. This review process helps ensure that taxpayers are reporting income correctly, claiming legitimate deductions, and paying the appropriate amount of taxes under federal law. Audits play an important role in maintaining fairness within the U.S. tax system because they help identify errors, prevent fraud, and encourage compliance.

Although the chances of being audited are relatively low for most taxpayers, understanding how audits work can help reduce fear and uncertainty. Whether you are an employee, freelancer, investor, small business owner, or self-employed professional, knowing what triggers an audit and how to respond can make the process far less stressful.

Understanding the Purpose of an IRS Audit

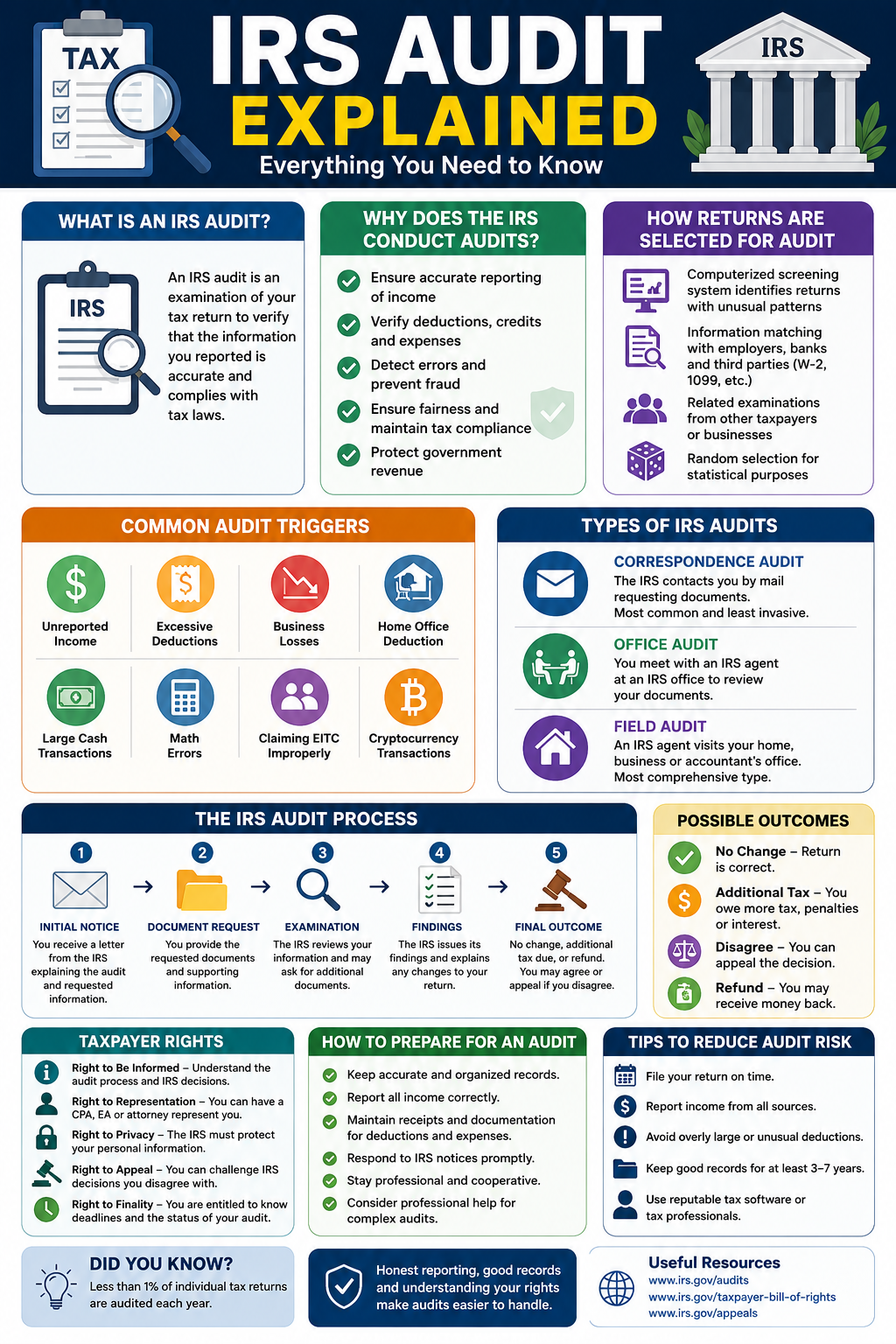

An IRS audit is an examination of a taxpayer’s financial information to determine whether the details reported on a tax return are accurate and comply with federal tax laws. During an audit, the IRS may review income records, deductions, credits, expenses, investments, business activities, and supporting documentation. The purpose is not necessarily to find wrongdoing but to verify that the return reflects the taxpayer’s actual financial situation.

The United States relies heavily on a voluntary compliance tax system. This means taxpayers are expected to calculate and report their taxes honestly without direct government involvement during the filing process. Because the IRS cannot manually review every tax return, it uses audits as a method of quality control. Audits help identify mistakes, correct inaccuracies, and ensure that tax laws are being followed consistently.

Many people mistakenly believe that audits only target wealthy individuals or businesses. While high-income taxpayers may face increased scrutiny in certain circumstances, audits can involve taxpayers from virtually any income level. Sometimes an audit occurs because of a simple reporting discrepancy rather than suspected fraud.

Understanding the purpose behind audits helps taxpayers view them as a verification process rather than an accusation. Most audits focus on specific issues and can be resolved through proper documentation and cooperation with IRS representatives.

Why the IRS Conducts Audits

The IRS conducts audits to maintain the integrity of the federal tax system. Every year, the federal government depends on tax revenue to fund public services, infrastructure projects, defense programs, healthcare initiatives, education support, and countless other government functions. To ensure that these programs receive appropriate funding, the IRS must verify that taxpayers are paying the correct amount of tax.

Audits also promote fairness among taxpayers. If some individuals intentionally underreport income or claim deductions they are not entitled to receive, they gain an unfair financial advantage over taxpayers who follow the rules. Audit programs help discourage such behavior and reinforce public confidence in the tax system.

Another reason audits are important is that they help identify trends in taxpayer errors. As tax laws evolve and new forms of income emerge, the IRS uses audit findings to improve guidance, education, and enforcement efforts. For example, the growth of cryptocurrency transactions and gig economy work has created new compliance challenges that require additional IRS attention.

How Tax Returns Are Selected for Audit

One of the most common misconceptions about IRS audits is that they occur randomly. While some returns are selected through random compliance studies, most audits result from specific indicators identified through sophisticated review systems.

The IRS uses advanced computer programs to analyze tax returns and identify patterns that may suggest inconsistencies or unusual reporting behavior. These systems compare returns against statistical norms for taxpayers with similar income levels, occupations, and financial situations. Returns that significantly deviate from expected patterns may receive additional scrutiny.

Information matching is another important audit selection tool. The IRS receives income reports from employers, banks, brokerage firms, payment processors, and other financial institutions. If the information reported by these third parties does not match what appears on a taxpayer’s return, the discrepancy may trigger further review.

Audits can also result from related examinations. For example, if a business is being audited and investigators discover questionable transactions involving vendors, contractors, or business partners, those individuals may become subject to examination as well.

While technology plays a major role in audit selection, human review remains important. Experienced IRS personnel evaluate potential audit cases and determine whether additional examination is warranted based on available information.

Common IRS Audit Triggers

Unreported Income

One of the most significant audit triggers is failing to report all taxable income. Because the IRS receives copies of many income-related documents directly from employers and financial institutions, discrepancies are often detected automatically.

Income sources that frequently create problems include freelance earnings, consulting fees, investment income, rental income, side business revenue, and cryptocurrency gains. Taxpayers sometimes assume that income reported on forms such as 1099s is optional or difficult for the IRS to track. In reality, these transactions are often among the easiest for the IRS to verify.

Even relatively small omissions can trigger notices or audits. Therefore, taxpayers should carefully review all income documents before filing and ensure that every taxable source is reported accurately.

Excessive Deductions

Claiming deductions is a legitimate way to reduce taxable income, but unusually large deductions can attract IRS attention. When deductions appear significantly higher than those claimed by taxpayers with similar income levels, the return may receive additional review.

Examples include unusually large charitable donations, excessive business expenses, substantial medical deductions, or large casualty loss claims. The IRS understands that legitimate circumstances can result in significant deductions, but taxpayers must be prepared to support those claims with proper documentation.

Maintaining receipts, invoices, canceled checks, acknowledgment letters, and other supporting records is essential when claiming substantial deductions.

Self-Employment and Business Losses

Self-employed individuals and small business owners often face increased audit risk because business income and expenses can be more difficult to verify than traditional wage income.

Businesses occasionally experience losses, particularly during startup periods. However, reporting losses year after year may cause the IRS to question whether the activity is a legitimate business or simply a hobby. The agency evaluates factors such as profitability, business planning, operational practices, and efforts to generate revenue.

Taxpayers operating businesses should maintain organized accounting records and separate personal finances from business activities whenever possible.

Home Office Deductions

The home office deduction has long been considered an audit trigger, although it remains a legitimate tax benefit for eligible taxpayers. To qualify, a portion of the home must be used regularly and exclusively for business purposes.

Problems often arise when taxpayers claim deductions for spaces that serve both personal and business functions. Maintaining clear documentation regarding the size and use of the workspace can help support the deduction if questions arise.

Cryptocurrency Transactions

The IRS has increased its focus on digital asset reporting in recent years. Cryptocurrency sales, exchanges, mining income, staking rewards, and certain digital asset transactions may have tax consequences.

Many taxpayers mistakenly assume that cryptocurrency transactions are anonymous or difficult for the IRS to track. However, reporting requirements continue to expand, and failure to disclose taxable digital asset activity can increase audit risk significantly.

Types of IRS Audits

Correspondence Audit

A correspondence audit is the most common and least intrusive type of IRS audit. These audits are conducted through mail and typically involve a specific issue rather than a comprehensive examination of the entire return.

The IRS sends a notice explaining what information is needed and requesting supporting documentation. Common issues include charitable contributions, education credits, dependency claims, and investment transactions.

Many correspondence audits are resolved quickly when taxpayers provide the requested records promptly and accurately.

Office Audit

An office audit requires the taxpayer to meet with an IRS examiner at a local IRS office. These audits generally involve more complex issues than correspondence audits and may require extensive documentation.

During the meeting, the examiner reviews records, asks questions, and evaluates supporting evidence. Taxpayers have the right to bring a representative such as a CPA, enrolled agent, or tax attorney to the meeting.

Office audits often focus on specific deductions, business expenses, or income reporting concerns.

Field Audit

Field audits are the most comprehensive form of IRS examination. In these cases, IRS representatives visit the taxpayer’s home, business, or accountant’s office to conduct an in-depth review.

Field audits are commonly used for businesses, high-income individuals, and situations involving complex financial activities. Examiners may review accounting systems, inventory records, payroll documentation, contracts, and other business records.

Because field audits can be extensive, professional representation is often highly beneficial.

What Happens During an IRS Audit?

The audit process begins when the IRS sends an official notice identifying the tax year under examination and the issues being reviewed. This notice outlines the documents required and provides instructions for responding.

Once the taxpayer receives the notice, gathering relevant records becomes a priority. Supporting documentation may include receipts, bank statements, invoices, payroll records, canceled checks, investment statements, mileage logs, and other financial evidence.

After reviewing submitted information, the IRS examiner evaluates whether the reported figures are accurate. Additional questions may arise during this phase, particularly if documentation is incomplete or raises new concerns.

At the conclusion of the audit, the IRS issues its findings. The examination may result in no changes, adjustments to the tax return, additional taxes owed, penalties, interest charges, or, in some cases, a refund.

Taxpayer Rights During an IRS Audit

The IRS Taxpayer Bill of Rights provides important protections throughout the audit process.

Taxpayers have the right to receive clear explanations regarding IRS decisions and procedures. They are entitled to understand why information is being requested and how the examination will proceed.

Individuals also have the right to professional representation. CPAs, enrolled agents, and tax attorneys may communicate with the IRS on behalf of taxpayers and assist in responding to audit inquiries.

Privacy rights ensure that audits are conducted appropriately and within legal boundaries. Taxpayers are protected from unnecessary intrusion and are entitled to fair treatment throughout the process.

If disagreements arise, taxpayers have the right to appeal audit findings. Administrative appeals and court proceedings provide opportunities to challenge decisions when necessary.

How to Prepare for an IRS Audit

Preparation can dramatically improve the audit experience. The most important step is maintaining organized records throughout the year rather than scrambling to locate documents after receiving an audit notice.

Taxpayers should retain copies of tax returns, income statements, receipts, invoices, mileage logs, bank statements, investment records, and other supporting documents. Digital storage systems can simplify organization and retrieval.

Responding promptly to IRS notices is equally important. Ignoring correspondence can lead to additional penalties and complications. Even if gathering records takes time, communicating with the IRS demonstrates cooperation and may prevent unnecessary problems.

Professional assistance can be valuable, particularly for complex audits involving businesses, investments, or substantial deductions. Experienced tax professionals understand IRS procedures and can help present information effectively.

Remaining professional and cooperative throughout the process often contributes to a smoother resolution. Emotional reactions or confrontational behavior rarely improve outcomes.

Possible Audit Outcomes

Many taxpayers assume that audits automatically result in additional taxes owed, but several outcomes are possible.

A no-change audit occurs when the IRS accepts the return as originally filed. In this situation, no adjustments are required, and the examination ends successfully.

An agreed adjustment occurs when the IRS proposes changes and the taxpayer accepts them. Additional taxes, penalties, or interest may apply depending on the circumstances.

If the taxpayer disagrees with the findings, the matter may proceed through the appeals process. Appeals provide an opportunity to present additional evidence and challenge IRS conclusions.

Occasionally, audits reveal that taxpayers overpaid taxes. In such cases, refunds may be issued if the taxpayer is entitled to additional credits, deductions, or adjustments.

Strategies for Reducing Audit Risk

While no taxpayer can eliminate audit risk completely, certain practices can significantly reduce the likelihood of problems.

Accurate reporting is essential. Carefully review tax returns before filing and ensure that income reported matches information provided by employers and financial institutions.

Maintain comprehensive documentation for deductions and credits. The stronger the records, the easier it becomes to support claims during an examination.

Avoid estimating expenses whenever possible. Actual records carry far more credibility than approximations.

Business owners should separate personal and business finances, maintain accurate accounting systems, and preserve supporting documentation for all significant transactions.

Using reputable tax preparation software or working with qualified tax professionals can also help identify errors before filing.

Frequently Asked Questions (FAQs)

What is the main purpose of an IRS audit?

The purpose of an IRS audit is to verify that information reported on a tax return is accurate and complies with federal tax laws.

How likely am I to be audited?

Most taxpayers have a relatively low chance of being audited, although risk levels vary based on income, deductions, and filing circumstances.

Does an audit mean I made a mistake?

No. Audits often result from routine review processes or reporting discrepancies and do not automatically indicate wrongdoing.

Can I represent myself during an audit?

Yes. However, taxpayers may also choose representation from a CPA, enrolled agent, or tax attorney.

How long should I keep tax records?

Generally, taxpayers should keep records for at least three years, though certain situations may require longer retention periods.

Can the IRS audit multiple years?

Yes. If issues are discovered, the IRS may examine additional tax years within applicable legal time limits.

What happens if I disagree with audit results?

Taxpayers have the right to appeal IRS findings through administrative appeals or the court system.

Are cryptocurrency transactions audited?

Yes. The IRS actively reviews cryptocurrency reporting and expects taxpayers to disclose taxable digital asset transactions.

References

- IRS Audit Information: https://www.irs.gov/businesses/small-businesses-self-employed/irs-audits

- Understanding Your IRS Audit: https://www.irs.gov/individuals/understanding-your-irs-audit

- Taxpayer Bill of Rights: https://www.irs.gov/taxpayer-bill-of-rights

- IRS Appeals Process: https://www.irs.gov/appeals

- IRS Publication 556: https://www.irs.gov/forms-pubs/about-publication-556

- IRS Recordkeeping Guide: https://www.irs.gov/businesses/small-businesses-self-employed/recordkeeping

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official authorities.