Buying a home for the first time is one of the biggest milestones in life. For many people in the United States, becoming a homeowner represents financial stability, long-term security, and personal achievement. However, the process of buying a house can also feel confusing and stressful, especially for first-time buyers who are unfamiliar with mortgages, down payments, closing costs, and loan requirements.

Over the past few years, rising home prices and increasing mortgage rates have made it more difficult for many Americans to enter the housing market. Because of this, first-time home buyer programs in the USA have become extremely important. These programs are designed to help people purchase homes with lower upfront costs, easier qualification requirements, and financial assistance that makes homeownership more affordable.

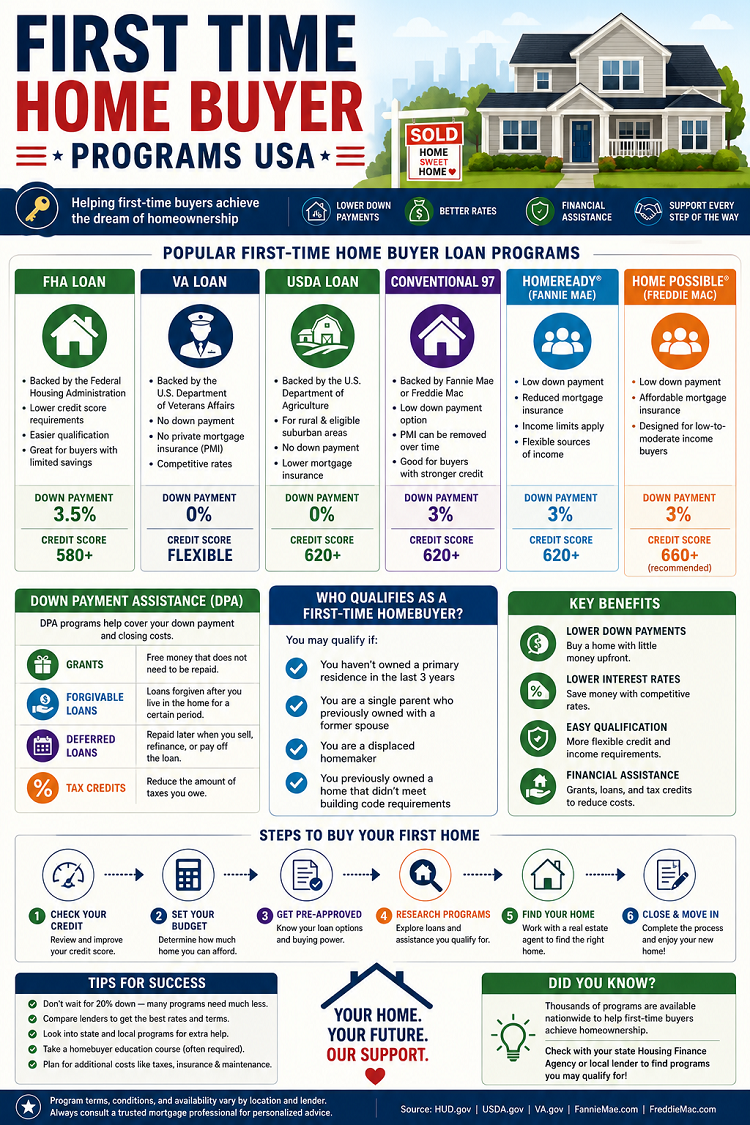

Many buyers still believe they need a perfect credit score and a 20% down payment to purchase a home. In reality, several loan programs allow qualified buyers to purchase homes with very little money down. Some government-backed mortgage programs even allow eligible buyers to purchase homes with zero down payment.

Overview of First Time Home Buyer Programs

| Program Type | Minimum Down Payment | Best For |

|---|---|---|

| FHA Loans | 3.5% | Buyers with lower credit |

| VA Loans | 0% | Veterans and military families |

| USDA Loans | 0% | Rural and suburban buyers |

| Conventional 97 | 3% | Buyers with stronger credit |

| Down Payment Assistance | Varies | Buyers needing financial help |

These programs exist because many people struggle to save enough money for a traditional mortgage. Housing costs, rent prices, student loans, and inflation have made saving for a home more challenging than ever before. First-time home buyer programs are designed to reduce these barriers and help more Americans achieve homeownership.

Some programs are backed directly by the federal government, while others are offered through state housing agencies, nonprofit organizations, or private lenders. Each program has different eligibility rules, benefits, and qualification standards, which means buyers should compare multiple options before deciding which loan best fits their needs.

What Is Considered a First Time Home Buyer?

A first-time home buyer is generally someone who has not owned a primary residence within the last three years. However, many people are surprised to learn that the definition is broader than they expected.

For example, you may still qualify as a first-time buyer if you previously owned a home with a former spouse or if your prior property did not meet current building standards. Some programs also consider displaced homemakers or individuals returning to the housing market after a long absence as first-time buyers.

Why First Time Home Buyer Programs Are Important

The cost of buying a home in the United States has increased dramatically in recent years. In many cities, average home prices are significantly higher than they were a decade ago. At the same time, rising rent costs have made it difficult for families to save enough money for a down payment.

Because of these financial challenges, first-time home buyer programs have become essential for many households. These programs help reduce upfront costs and make mortgage approval more accessible for buyers with moderate income or limited savings.

Without these programs, many people would need to wait years before they could afford to purchase a home. Instead of requiring huge down payments, modern mortgage programs allow buyers to enter the housing market sooner and begin building equity earlier in life.

Benefits of First Time Home Buyer Programs

Lower Down Payments

One of the biggest reasons buyers use these programs is because of the lower down payment requirements.

Traditional mortgages often required buyers to save 20% of the home price before qualifying for a loan. For many Americans, saving tens of thousands of dollars while paying rent and other living expenses is extremely difficult.

Modern mortgage programs have changed this significantly. Some loans now allow buyers to purchase homes with as little as 3% down, while others offer zero-down-payment options.

| Home Price | 20% Down | 3% Down |

|---|---|---|

| $300,000 | $60,000 | $9,000 |

| $450,000 | $90,000 | $13,500 |

This difference allows buyers to purchase homes much sooner instead of spending years trying to save a massive down payment.

Flexible Credit Score Requirements

Another major advantage is flexible credit standards. Many first-time buyers worry that past financial mistakes will prevent them from qualifying for a mortgage.

Government-backed loans are often more forgiving than traditional mortgage products. Buyers with moderate credit scores may still qualify if they have stable income and manageable debt.

This flexibility helps people who may have experienced:

- Medical debt

- Student loan balances

- Credit card debt

- Limited credit history

- Temporary financial hardship

Improving your credit score before applying can still help secure better interest rates, but buyers do not always need perfect credit to qualify for a home loan.

Financial Assistance and Grants

Many first-time buyers are unaware that financial assistance programs exist in nearly every state.

These programs may help cover:

- Down payments

- Closing costs

- Mortgage fees

- Interest rate reductions

Some assistance programs provide grants that never need to be repaid. Others offer forgivable loans that disappear after living in the home for a certain number of years.

This assistance can dramatically reduce the amount of money buyers need upfront, making homeownership possible for households with moderate income.

FHA Loans Guide

VA Loans Guide

A VA Loans Guide explains how veterans and active military members can access affordable home financing options. It covers eligibility requirements, key benefits, and the basic loan application process

USDA Loans Guide

The USDA Loans Guide helps buyers understand low-cost home loan opportunities available in eligible rural areas. It provides simple information about qualifications, advantages, and how to apply for a USDA backed mortgage.

Down Payment Assistance

Down Payment Assistance programs help home buyers reduce the upfront cost of purchasing a home. These programs offer grants or low-interest support to make homeownership more affordable and accessible.

Conventional Mortgage Programs

Conventional mortgages are loans offered through private lenders rather than government agencies. These loans are often best suited for buyers with stronger credit profiles and stable financial histories.

Although conventional loans were once associated with large down payments, several modern programs now allow buyers to purchase homes with as little as 3% down.

One major advantage of conventional mortgages is that private mortgage insurance can often be removed once the homeowner builds enough equity in the property.

Buyers with higher credit scores may also qualify for lower interest rates compared to government-backed loans.

Mortgage Pre Approval Process

Mortgage pre approval is one of the most important steps in the home-buying journey. During this process, lenders evaluate the buyer’s financial information to determine how much they are willing to lend.

Lenders usually review:

- Income

- Employment history

- Credit score

- Debt obligations

- Savings

- Tax returns

Pre-approval gives buyers a realistic understanding of their budget and strengthens their position when making offers on homes.

Sellers often prefer buyers who are already pre-approved because it shows financial readiness and reduces the risk of financing problems later in the process.

Understanding Closing Costs

Many first-time buyers focus only on the down payment and forget about closing costs.

Closing costs are additional fees paid during the final stage of the home purchase. These expenses may include:

- Lender fees

- Title insurance

- Property taxes

- Home insurance

- Appraisal costs

- Attorney fees

Closing costs typically range between 2% and 5% of the home price.

Understanding these costs ahead of time helps buyers avoid unexpected financial stress during closing.

Common Mistakes First Time Buyers Make

Waiting for a Perfect Market

Many buyers delay purchasing because they hope interest rates or home prices will fall significantly.

While market conditions matter, waiting too long can sometimes result in higher prices and reduced affordability.

Buying More House Than They Can Afford

Just because a lender approves a certain loan amount does not mean buyers should spend the maximum possible amount.

A comfortable monthly payment is usually more important than purchasing the largest house available.

Ignoring Emergency Savings

Some buyers spend all their savings on the purchase and have little money left for emergencies or repairs.

Maintaining a financial safety cushion after moving into a home is extremely important.

State Housing Assistance Programs

Nearly every U.S. state offers some form of housing assistance for first-time buyers.

These programs may provide:

- Down payment grants

- Reduced mortgage interest rates

- Tax incentives

- Closing cost help

Eligibility requirements vary by location, income level, and home price limits.

Because state programs change frequently, buyers should research local housing agencies for updated information.

Frequently Asked Questions

What is the best loan for first-time home buyers?

The best loan depends on your financial situation. FHA loans are popular for lower credit scores, while VA and USDA loans offer zero-down-payment options for eligible buyers.

Can I buy a house with no down payment?

Yes. VA loans and USDA loans may allow qualified buyers to purchase homes without a down payment.

Do first-time buyers need perfect credit?

No. Many programs allow buyers with moderate credit scores to qualify if they meet income and debt requirements.

How much money should I save before buying a home?

Besides the down payment, buyers should also prepare for closing costs, moving expenses, and emergency repairs.

Are down payment assistance programs free?

Some programs are grants that never require repayment, while others may involve forgivable or deferred loans.

References

- HUD Home Buying Resources

- Federal Housing Administration (FHA)

- VA Home Loans Program

- USDA Rural Development Housing Programs

- Freddie Mac Home Possible Program

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official authorities.