Retirement planning is one of the most important financial responsibilities people face during their working years. Unfortunately, millions of workers delay retirement savings because they believe they do not earn enough money to invest for the future. Others assume retirement accounts are only useful for wealthy individuals. In reality, the U.S. tax system includes several incentives specifically designed to help low-income and middle-income workers build retirement savings. One of the most valuable but overlooked incentives is the Retirement Contribution Credit, commonly called the Saver’s Credit.

The Retirement Contribution Credit rewards eligible taxpayers who contribute money to qualified retirement accounts such as IRAs and employer-sponsored retirement plans. Instead of simply reducing taxable income like a deduction, this credit directly lowers the amount of taxes owed. That means qualified taxpayers can save money immediately while simultaneously building long-term retirement wealth.

For many households, especially families living on moderate incomes, every tax dollar matters. The Saver’s Credit can make retirement contributions more affordable and encourage better long-term financial habits. Individuals who qualify may receive hundreds or even thousands of dollars in tax savings each year simply by contributing to retirement accounts they may already use.

This comprehensive guide explains how retirement contribution credits work, who qualifies, eligible retirement accounts, income limits, tax rules, planning strategies, and ways to maximize long-term financial benefits. Whether you are a beginner starting your first retirement account or an experienced saver looking to optimize tax advantages, understanding retirement contribution credits can significantly improve your financial future.

What Is the Retirement Contribution Credit?

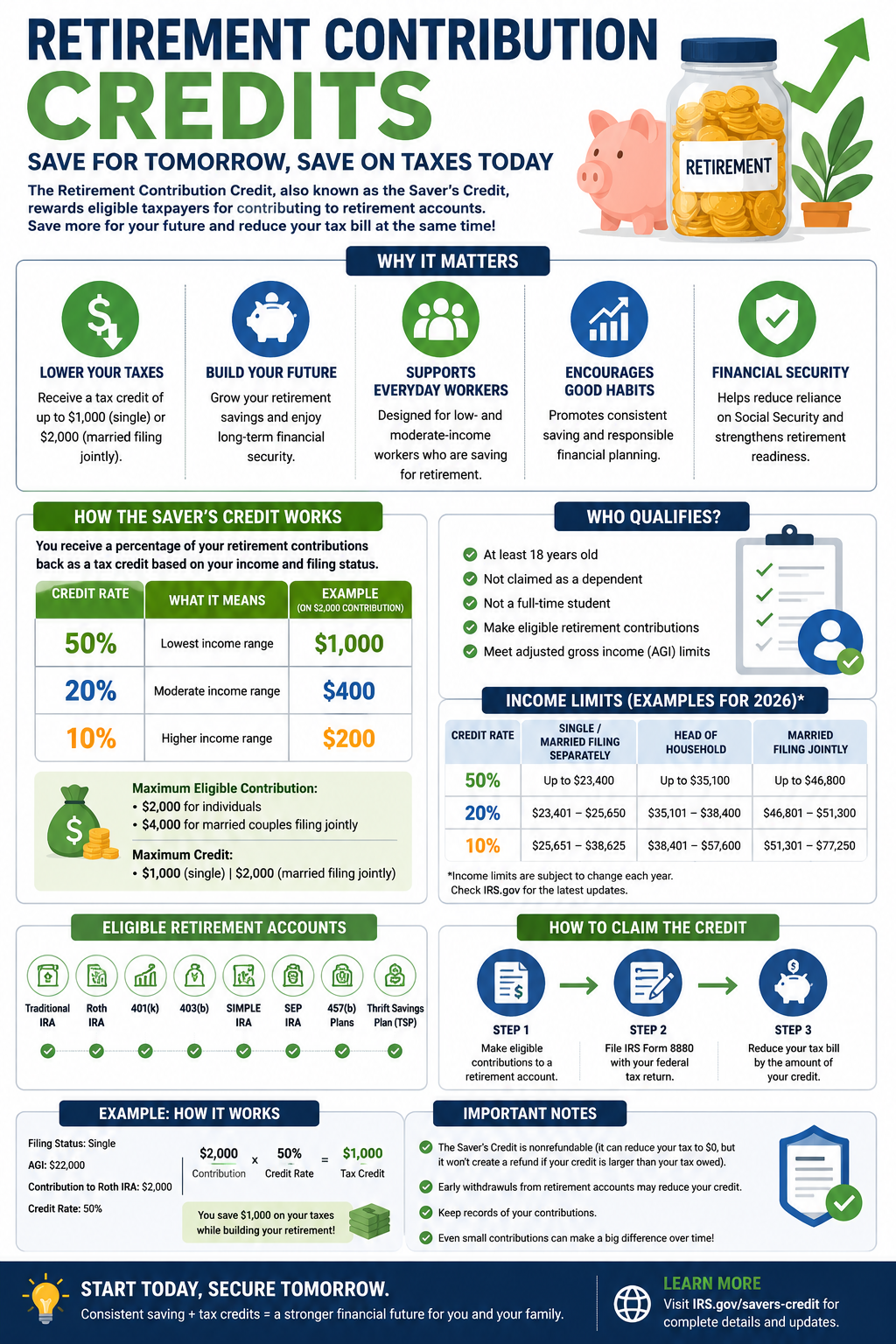

The Retirement Contribution Credit, officially called the Retirement Savings Contributions Credit, is a federal tax credit available to eligible taxpayers who contribute to qualified retirement accounts. Most people know it as the Saver’s Credit because it encourages Americans to save for retirement.

The purpose of the credit is simple: the government wants more people to save money for retirement instead of depending entirely on Social Security or public assistance programs later in life. To motivate retirement savings, lawmakers created a tax incentive that rewards individuals for contributing to retirement plans.

Unlike a tax deduction, which only lowers taxable income, a tax credit directly reduces the amount of taxes you owe. This distinction is extremely important because credits are often more valuable than deductions, especially for lower-income taxpayers.

For example, imagine two different taxpayers each contribute $2,000 to a retirement account. One taxpayer receives only a deduction, while the other qualifies for a 50% Saver’s Credit. The taxpayer receiving the credit could reduce their tax bill by as much as $1,000 directly, which provides much stronger immediate savings.

The Saver’s Credit is designed mainly for workers with low or moderate incomes. Eligibility depends on factors such as income level, filing status, age, student status, and retirement contributions made during the tax year.

Key Reasons the Saver’s Credit Matters

1. Encourages Long-Term Financial Security

Many people postpone retirement savings because they focus on short-term expenses. The Saver’s Credit creates a strong incentive to start investing for the future sooner rather than later.

2. Provides Immediate Tax Relief

Contributing to retirement accounts can reduce taxes in two ways:

- Through deductions

- Through tax credits

The Saver’s Credit directly lowers tax liability, which can provide meaningful savings during tax season.

3. Helps Lower-Income Workers Build Wealth

The credit specifically targets lower-income and middle-income workers who often struggle to save consistently. It rewards disciplined financial behavior and encourages long-term planning.

4. Supports Retirement Independence

Individuals with stronger retirement savings are less likely to rely entirely on Social Security benefits later in life. This creates greater financial independence and flexibility during retirement years.

5. Promotes Better Financial Habits

People who regularly contribute to retirement accounts often develop healthier financial habits overall, including budgeting, investing, and long-term planning.

How the Retirement Contribution Credit Works

The Saver’s Credit works by giving eligible taxpayers a percentage of their retirement contributions back as a tax credit.

The credit percentage depends mainly on income and filing status. Eligible taxpayers may receive a credit worth:

- 50% of contributions

- 20% of contributions

- 10% of contributions

The lower your income, the higher your potential credit percentage.

The maximum amount of retirement contributions eligible for the credit is generally:

- $2,000 for individuals

- $4,000 for married couples filing jointly

This means the maximum credit available is usually:

| Filing Status | Maximum Credit |

|---|---|

| Single | $1,000 |

| Married Filing Jointly | $2,000 |

Simple Saver’s Credit Example

Suppose a taxpayer contributes $2,000 to a Roth IRA and qualifies for the 50% credit rate.

The calculation would be:

0.50×2000=10000.50 \times 2000 = 1000

The taxpayer would receive a $1,000 reduction in taxes owed.

That represents a major financial incentive for contributing to retirement savings.

Married Couple Example

Assume a married couple contributes:

- Spouse A: $2,000

- Spouse B: $2,000

Their total eligible contributions equal:

2000+2000=40002000 + 2000 = 4000

If they qualify for the 50% Saver’s Credit rate:

0.50×4000=20000.50 \times 4000 = 2000

The couple could reduce their tax bill by $2,000.

Who Qualifies for Retirement Contribution Credits?

Not everyone qualifies for the Saver’s Credit. The IRS applies several eligibility rules.

To qualify, taxpayers generally must:

- Be at least 18 years old

- Not be claimed as a dependent

- Not be a full-time student

- Make eligible retirement contributions

- Meet adjusted gross income (AGI) limits

These rules are intended to focus the credit on working adults who are building retirement savings independently.

Income Limits for Saver’s Credit

Income limits change periodically because of inflation adjustments. Eligibility depends on adjusted gross income and filing status.

Taxpayers with lower incomes qualify for higher credit percentages.

General Saver’s Credit Structure

| Credit Percentage | Income Level |

|---|---|

| 50% | Lowest income range |

| 20% | Moderate income range |

| 10% | Higher qualifying range |

Workers above certain income thresholds do not qualify.

You should always review updated IRS guidelines for the latest income limits.

Reference:

- IRS Saver’s Credit Information: IRS Saver’s Credit Resource

Eligible Retirement Accounts

Several retirement plans qualify for the Saver’s Credit.

Common Eligible Accounts

| Retirement Account | Eligible |

|---|---|

| Traditional IRA | Yes |

| Roth IRA | Yes |

| 401(k) | Yes |

| 403(b) | Yes |

| SIMPLE IRA | Yes |

| SEP IRA | Yes |

| Governmental 457(b) | Yes |

| Thrift Savings Plan (TSP) | Yes |

These accounts are designed to encourage retirement saving and often include additional tax advantages.

Traditional IRA and the Saver’s Credit

Traditional IRAs remain one of the most popular retirement accounts in the United States.

Contributions to Traditional IRAs may provide:

- Tax deductions

- Tax-deferred growth

- Saver’s Credit eligibility

This creates a double tax benefit for some taxpayers.

For example, a taxpayer might reduce taxable income with an IRA deduction while also receiving a Saver’s Credit based on contributions.

This combination can substantially lower taxes owed.

Roth IRA Contributions and Retirement Credits

Roth IRAs are also eligible for the Saver’s Credit even though Roth contributions are made with after-tax dollars.

Benefits of Roth IRAs include:

- Tax-free qualified withdrawals

- No tax on investment growth

- Flexible retirement income planning

- No required minimum distributions during the original owner’s lifetime

The Saver’s Credit makes Roth IRAs even more attractive for younger workers and moderate-income earners.

Employer-Sponsored Retirement Plans

Many workers contribute to retirement accounts directly through their employers.

Eligible employer-sponsored plans include:

- 401(k)

- 403(b)

- SIMPLE IRA

- Governmental 457(b)

Payroll deductions into these plans can qualify for the Saver’s Credit.

Some employers also provide matching contributions, which increase retirement savings even further.

Employer Matching Contributions

Employer matching is one of the best retirement benefits available.

For example, an employer may match 50% or 100% of employee retirement contributions up to a certain limit.

This means workers can potentially receive:

- Tax savings

- Saver’s Credit benefits

- Employer matching contributions

- Long-term investment growth

Together, these advantages create powerful wealth-building opportunities.

Self-Employed Workers and Retirement Credits

Self-employed individuals can also qualify for retirement contribution credits.

This includes:

- Freelancers

- Contractors

- Gig workers

- Small business owners

- Consultants

Popular self-employed retirement plans include:

| Retirement Plan | Common Users |

|---|---|

| SEP IRA | Small business owners |

| Solo 401(k) | Independent workers |

| SIMPLE IRA | Small employers |

Self-employed workers often overlook retirement tax credits, but these benefits can significantly reduce taxes while building future wealth.

Why Starting Early Matters

One of the most important concepts in retirement planning is compound growth.

When money remains invested over long periods, investment earnings begin generating additional earnings.

This creates exponential long-term growth.

Compound Interest Formula

Suppose you invest:

- Principal = $5,000

- Interest rate = 6% annually

- Compounded monthly

- Time = 10 years

The calculation becomes:

A=5000(1+0.0612)12×10A=5000\left(1+\frac{0.06}{12}\right)^{12\times10}

After solving, the investment grows significantly because interest keeps compounding over time.

Example of Long-Term Retirement Growth

Suppose someone contributes $200 per month starting at age 25 instead of waiting until age 35.

Because of compound growth, the early saver may accumulate significantly more retirement wealth even if total contributions are similar.

The Saver’s Credit encourages workers to start saving earlier, which improves long-term outcomes dramatically.

Common Mistakes Taxpayers Make

Many eligible taxpayers fail to claim the Saver’s Credit simply because they do not know it exists.

Others make filing errors that prevent them from receiving benefits.

Common Mistakes Include

| Mistake | Consequence |

|---|---|

| Forgetting IRS Form 8880 | Credit not claimed |

| Missing contribution deadlines | Contributions excluded |

| Exceeding income limits | Credit reduced or eliminated |

| Taking early withdrawals | Contribution amount reduced |

| Assuming Roth IRAs do not qualify | Lost tax savings |

Proper tax planning helps avoid these issues.

How to Claim the Saver’s Credit

Taxpayers generally claim the credit by filing:

- Federal income tax return

- IRS Form 8880

IRS Form 8880 calculates:

- Eligible contributions

- Applicable credit rate

- Final credit amount

Contribution Deadlines

IRA contributions for a tax year are usually allowed until the federal tax filing deadline.

Employer-sponsored retirement plans typically follow payroll contribution schedules.

Taxpayers should verify all deadlines carefully to avoid losing eligibility.

Saver’s Credit Is Nonrefundable

The Retirement Contribution Credit is generally nonrefundable.

This means:

- It can reduce taxes owed to zero

- It usually cannot generate a refund larger than total taxes owed

Although refundable credits are often more valuable, the Saver’s Credit still provides meaningful tax reductions.

Retirement Contribution Strategies

Maximizing retirement contribution credits requires careful financial planning.

Smart Strategies Include

Contribute Consistently

Regular contributions create discipline and maximize long-term investment growth.

Use Automatic Payroll Deductions

Automation makes retirement saving easier and reduces the temptation to spend money elsewhere.

Increase Contributions Gradually

Small annual increases can dramatically improve retirement savings over time.

Coordinate Contributions With a Spouse

Married couples may increase combined Saver’s Credit benefits through coordinated planning.

Lower Adjusted Gross Income

Reducing AGI through deductions or retirement contributions may help taxpayers qualify for larger credits.

Retirement Savings and Inflation

Inflation steadily reduces purchasing power over time.

Without adequate retirement savings, future living expenses may become difficult to manage.

Retirement accounts help combat inflation through long-term investment growth and compound returns.

Importance of Financial Literacy

Many workers lack basic retirement planning knowledge.

Improved financial literacy helps people:

- Understand retirement accounts

- Use tax advantages effectively

- Avoid debt problems

- Invest more consistently

- Prepare for long-term financial needs

Retirement Challenges Facing Modern Workers

Modern workers face numerous financial pressures, including:

- Rising housing costs

- Healthcare expenses

- Student loans

- Inflation

- Childcare costs

These challenges make retirement saving difficult, especially for younger households.

Retirement Planning for Younger Workers

Young adults often believe retirement planning can wait until later in life.

However, delaying retirement savings can dramatically reduce long-term wealth accumulation.

Even small early contributions can grow substantially because of compound returns.

The Saver’s Credit provides extra motivation for younger workers to begin saving sooner.

Retirement Planning for Families

Families balancing mortgages, childcare, and education expenses may struggle to prioritize retirement savings.

Still, even modest contributions can provide:

- Tax credits

- Long-term growth

- Financial security

- Retirement independence

Building retirement savings gradually is often more effective than waiting for a “perfect” financial situation.

Retirement Contribution Credits and Economic Stability

Encouraging retirement savings benefits not only individuals but also the broader economy.

Workers with stronger retirement savings are less dependent on government assistance and often contribute to healthier financial systems overall.

Higher retirement savings can improve:

- Consumer confidence

- Long-term investment markets

- Household financial stability

- Economic resilience

State Tax Benefits for Retirement Contributions

Some states offer additional tax incentives for retirement savings.

Potential benefits include:

- State income tax deductions

- Retirement exclusions

- Tax-deferred investment treatment

Rules vary by state, so taxpayers should review local tax laws carefully.

Best Retirement Accounts for Beginners

Choosing the right retirement account depends on factors such as income, employer benefits, and long-term goals.

Common Beginner Options

| Account Type | Main Benefit |

|---|---|

| 401(k) | Employer matching |

| Roth IRA | Tax-free retirement withdrawals |

| Traditional IRA | Potential tax deduction |

Many financial experts recommend contributing enough to employer plans to receive full employer matching before investing elsewhere.

Future of Retirement Savings Incentives

Governments continue searching for ways to improve retirement readiness among workers.

Future changes could include:

- Expanded Saver’s Credit eligibility

- Higher contribution limits

- Automatic retirement enrollment systems

- Greater financial education programs

As retirement challenges grow, tax incentives will likely remain an important policy tool.

Frequently Asked Questions (FAQs)

What is the Retirement Contribution Credit?

The Retirement Contribution Credit, also known as the Saver’s Credit, is a federal tax credit that rewards eligible taxpayers for contributing to retirement savings accounts.

Who can qualify for the Saver’s Credit?

Eligible taxpayers must generally:

- Be at least 18 years old

- Not be full-time students

- Not be claimed as dependents

- Meet income requirements

- Make eligible retirement contributions

Which retirement accounts qualify?

Eligible accounts usually include:

- Traditional IRA

- Roth IRA

- 401(k)

- SIMPLE IRA

- SEP IRA

- 403(b)

- Governmental 457(b)

Is the Saver’s Credit refundable?

No. The Saver’s Credit is generally nonrefundable.

Can I receive both a deduction and a Saver’s Credit?

Yes. Some taxpayers qualify for both an IRA deduction and the Saver’s Credit.

What is the maximum Saver’s Credit amount?

The maximum credit is generally:

- $1,000 for individuals

- $2,000 for married couples filing jointly

Do Roth IRA contributions qualify?

Yes. Roth IRA contributions may qualify for the Saver’s Credit.

How do I claim the Saver’s Credit?

Taxpayers usually claim the credit using IRS Form 8880 when filing federal income taxes.

Can self-employed individuals qualify?

Yes. Self-employed workers contributing to eligible retirement plans may qualify.

Do early withdrawals affect the credit?

Yes. Certain retirement account withdrawals may reduce eligible contribution amounts.

References

- IRS Saver’s Credit Guide: IRS Retirement Savings Contributions Credit Page

- IRS Form 8880 Instructions: IRS Form 8880 Resource

- U.S. Department of Labor Retirement Information: Department of Labor Retirement Topics

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official authorities.