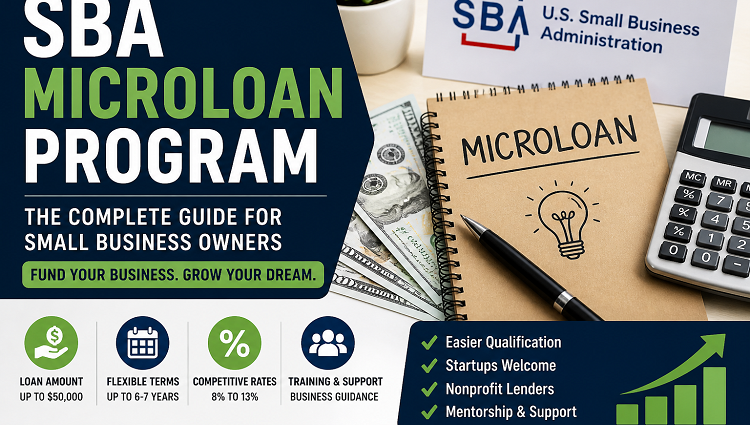

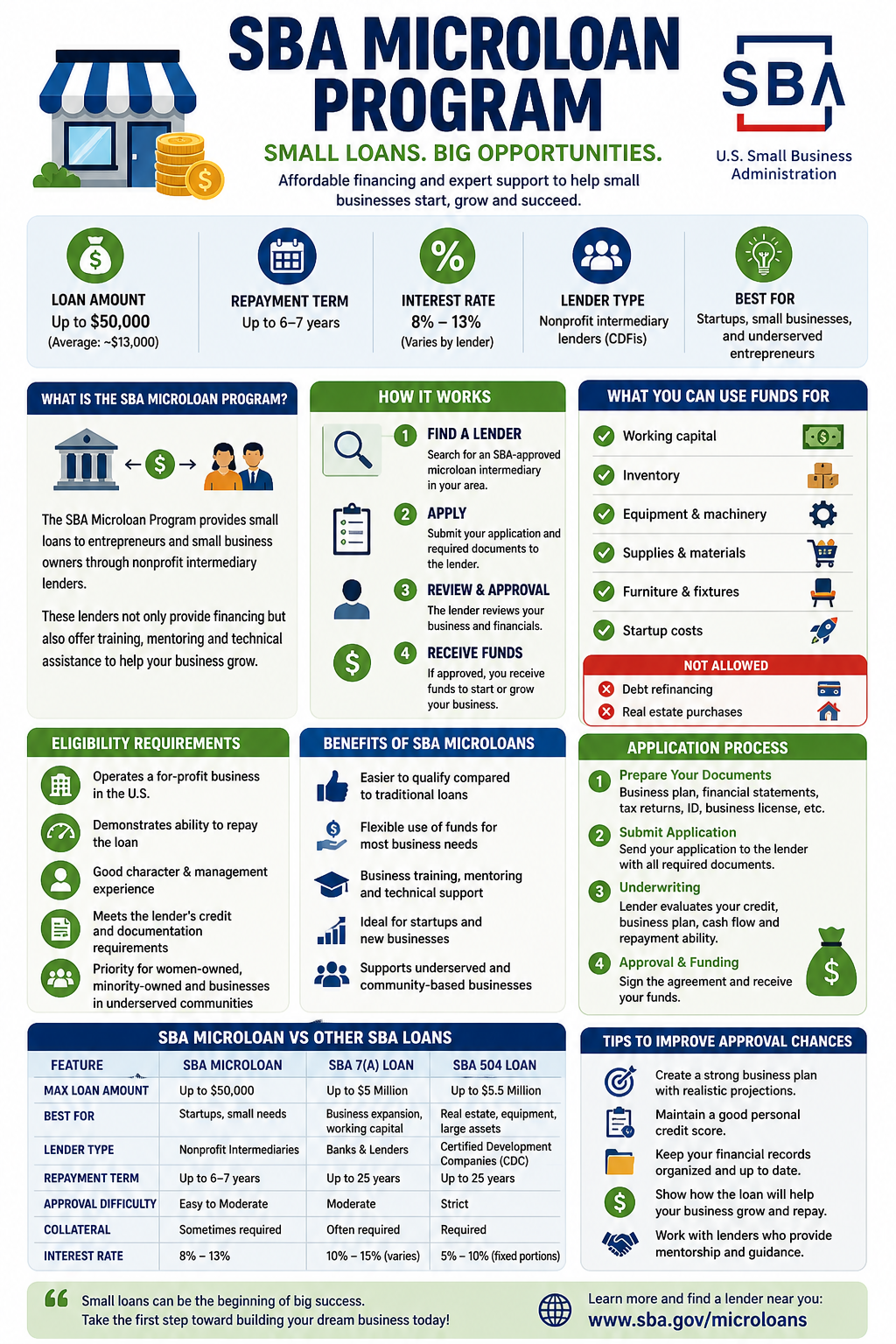

The SBA Microloan Program is one of the most important small business funding initiatives in the United States, especially for startups and entrepreneurs who struggle to access traditional bank financing. It is designed to provide small, manageable loans up to $50,000 along with training and guidance to help businesses grow sustainably. Unlike large commercial loans that focus heavily on credit history and collateral, the SBA Microloan Program takes a more community-driven and supportive approach, making it ideal for first-time business owners and underserved entrepreneurs.

This guide explains the SBA Microloan Program in extreme detail, including how it works, eligibility rules, application process, advantages, disadvantages, and strategies to improve approval chances. Everything is written in a structured, SEO-optimized format to help you fully understand the program from start to finish.

SBA Microloan Program

The U.S. Small Business Administration (SBA) created the Microloan Program to support small businesses that need relatively small amounts of capital but still struggle to access financing through banks or credit unions. Instead of directly lending money, the SBA works through intermediary nonprofit lenders, which distribute the funds and also provide training and advisory services.

These intermediaries are often Community Development Financial Institutions (CDFIs) or local nonprofit organizations focused on economic development. Their goal is not only to provide loans but also to help entrepreneurs build long-term financial stability.

The SBA itself provides funding to these intermediaries, which then lend to small business owners based on their own evaluation criteria. This structure allows for more flexibility compared to traditional lending systems.

According to the SBA, microloans are specifically intended for:

- Startup businesses

- Expanding small businesses

- Women-owned businesses

- Minority-owned businesses

- Low-income or underserved communities

Loan Amount and Financial Structure

The SBA Microloan Program is designed for small-scale funding needs, which is why the loan amounts are relatively modest compared to other SBA programs.

The maximum loan amount is $50,000, but most borrowers receive significantly less, with the average loan being around $13,000. This makes it ideal for micro-level business operations rather than large-scale expansion projects.

The repayment structure is typically more flexible than traditional bank loans. Borrowers usually get a repayment term of up to 6 to 7 years, depending on the lender’s terms and the borrower’s financial situation.

Interest rates generally fall between 8% and 13%, which may vary based on risk assessment, credit history, and lender policies.

Funds can be used for a wide variety of business purposes, including:

- Working capital for daily operations

- Purchasing inventory or raw materials

- Buying machinery or equipment

- Furniture and office setup

- Startup costs for new businesses

However, there are restrictions. SBA microloans cannot be used for:

- Paying off existing debts

- Purchasing real estate or property

- Personal non-business expenses

This ensures that funds are strictly used for business development.

How SBA Microloans Actually Work

Many people assume the SBA directly gives loans, but that is not how the system operates. Instead, the SBA functions as a funding and regulatory body, while actual lending is done through approved intermediaries.

Here is how the system works in detail:

First, the SBA allocates funds to nonprofit intermediary lenders. These organizations are carefully selected based on their experience in community lending and business development.

Next, these intermediaries accept loan applications directly from small business owners. They evaluate each application based on business viability, credit history, repayment ability, and overall risk.

If the application is approved, the intermediary issues the loan directly to the borrower, not the SBA. The borrower then repays the loan back to the intermediary, which in turn manages the repayment cycle according to SBA guidelines.

This system is designed to create a community-based lending environment, where lenders not only provide money but also offer mentorship and training.

Requirements for SBA Microloans

Eligibility for SBA Microloans is more flexible compared to traditional bank loans, but applicants still need to meet certain criteria.

To qualify, you generally must be operating a small business in the United States. Startups are also eligible, which makes this program particularly attractive for new entrepreneurs who do not yet have a financial track record.

Lenders typically evaluate several factors:

Credit Score

While there is no strict minimum requirement set by the SBA, most lenders prefer a credit score of around 600–650 or higher. However, some nonprofit lenders may accept lower scores if other factors are strong.

Business Plan

A well-written business plan is extremely important. It should clearly explain:

- Business model

- Market analysis

- Revenue projections

- Cost structure

- Growth strategy

Ability to Repay

Lenders will assess your cash flow projections to determine whether your business can realistically repay the loan.

Experience

Prior business or industry experience can significantly improve approval chances.

Collateral

Collateral is not always required, but some lenders may ask for partial security depending on the loan amount and risk level.

The SBA Microloan Program is particularly focused on supporting:

- Women entrepreneurs

- Minority business owners

- Low-income communities

- First-time business owners

Advantages of SBA Microloan Program

The SBA Microloan Program offers several major advantages that make it one of the most accessible funding options in the U.S. small business ecosystem.

One of the biggest benefits is accessibility. Many small businesses and startups are rejected by traditional banks due to lack of credit history or insufficient collateral. SBA microloans fill this gap by offering more flexible approval criteria.

Another major advantage is the support system. Unlike traditional loans, microloan intermediaries often provide training, business mentoring, and financial guidance. This helps entrepreneurs not only receive funding but also learn how to manage and grow their businesses effectively.

The program is also highly beneficial for startups, which typically struggle to secure funding during early stages. Since SBA microloans do not require a long financial history, they are ideal for new entrepreneurs.

Additionally, the loan structure is relatively flexible, with repayment terms extending up to 7 years, making monthly payments more manageable.

Limitations and Challenges

Despite its benefits, the SBA Microloan Program also has some limitations that applicants should understand clearly.

The most obvious limitation is the loan size cap of $50,000, which may not be sufficient for businesses requiring large capital investments. This makes the program unsuitable for large-scale expansion projects.

Another limitation is that loan usage is restricted strictly to business purposes, meaning it cannot be used for debt consolidation or real estate purchases.

The application process can also be time-consuming because each intermediary lender has its own evaluation system, which may lead to delays in approval and funding.

In some cases, lenders may require collateral or a personal guarantee, which increases financial risk for the borrower.

SBA Microloan vs Other Small Business Loans

| Feature | SBA Microloan | SBA 7(a) Loan | SBA 504 Loan | Traditional Bank Loan |

|---|---|---|---|---|

| Maximum Loan Amount | Up to $50,000 | Up to $5 million | Up to $5.5 million | Varies (often $10K–$1M+) |

| Average Loan Size | Around $13,000 | $100,000–$500,000+ | $500,000+ | Depends on borrower profile |

| Loan Purpose | Startup costs, working capital, inventory, equipment | General business funding, expansion, refinancing | Real estate, machinery, large assets | Broad business needs |

| Lender Type | Nonprofit intermediaries (CDFIs) | Banks, credit unions, SBA lenders | Certified Development Companies | Banks & financial institutions |

| Approval Difficulty | Easy to moderate | Moderate | Strict | Strict |

| Credit Requirements | Flexible (often 600+) | Good credit required (650–700+) | Strong credit required | Very strong credit required |

| Collateral Requirement | Sometimes required | Often required | Required | Usually required |

| Interest Rate | ~8%–13% | ~10%–15% (varies) | ~5%–10% (fixed portions) | ~6%–12% |

| Repayment Term | Up to 6–7 years | Up to 25 years | Up to 25 years | 1–20 years |

| Best For | Startups, small businesses, underserved entrepreneurs | Growing established businesses | Real estate & large equipment purchases | Businesses with strong financial history |

| Speed of Funding | Medium (2–8 weeks) | Medium | Slow | Fast to medium |

To understand the value of SBA microloans, it is useful to compare them with other SBA loan programs.

The SBA 7(a) loan program offers much larger funding up to $5 million but requires stronger credit history and financial documentation. It is better suited for established businesses.

The SBA 504 loan program is designed for major fixed asset purchases like real estate and equipment, with strict eligibility requirements.

In contrast, the SBA Microloan Program is much smaller in scale but significantly easier to access, making it ideal for startups and micro-businesses.

Application Process

Applying for an SBA Microloan involves several steps, each of which is important for approval success.

First, you must find an SBA-approved intermediary lender in your region. These lenders are listed on the SBA official website.

Next, you prepare your documentation, which typically includes:

- Business plan

- Financial statements

- Personal tax returns

- Cash flow projections

- Legal business registration documents

After that, you submit your application directly to the lender. They will review your financial profile, business idea, and repayment ability.

If your application passes the initial review, it goes through underwriting, where deeper financial analysis is conducted.

Finally, if approved, you sign the loan agreement and receive funds directly from the lender.

Common Mistakes That Lead to Rejection

Many applicants are rejected due to avoidable mistakes. One of the most common issues is submitting a weak or incomplete business plan. Without clear financial projections and market analysis, lenders may view the business as high risk.

Another common mistake is ignoring credit preparation. Even though credit requirements are flexible, extremely poor credit can still reduce approval chances.

Incomplete documentation is also a frequent reason for delays or rejection. Lenders require accurate financial records to evaluate risk properly.

Frequently Asked Questions (FAQs)

What is the SBA Microloan maximum amount?

The maximum loan amount is $50,000, although most loans are smaller.

Can startups apply for SBA Microloans?

Yes, startups are one of the primary target groups of this program.

How long does approval take?

Approval time varies depending on the lender but can range from a few weeks to several months.

Is collateral required?

Collateral may be required depending on the lender and loan size.

What is the interest rate?

Interest rates typically range between 8% and 13%.

Reference Links

- https://www.sba.gov/microloans

- https://www.sba.gov/business-guide/plan-your-business/financing-your-business

- https://www.nerdwallet.com/article/small-business/sba-microloans

- https://www.wsj.com/buyside/personal-finance/business-loans/sba-loans-overview

Disclaimer

Program Clarity is an independent informational website and is not affiliated with any government agency. This article is for educational purposes only. Program rules and availability may change. Always verify details with official authorities.